| |

CDJ 2026 Kar HC 527

|

| Court : High Court of Karnataka |

| Case No : Writ Petition Nos. 19885, 15749, 19226, 21870, 22068, 26387, 26522, 27096, 29267, 29408, 29502, 29776, 30785, 31714, 32436, 32451, 32829, 32843 Of 2025 (L-PF) etc., |

| Judges: THE HONOURABLE MR. JUSTICE ANANT RAMANATH HEGDE |

| Parties : Bharath Earth Movers Employees Association, Represented By Its President, M. Mahesh, Bangalore & Others Versus Union Of India, Department Of Ministry Of Labour & Employment, Government Of India, Represented By Its Secretary, New Delhi & Others |

| Appearing Advocates : For the Appearing Parties: Harish Narasappa, Senior Counsel, S. Yathish, M.R. Varun, K. Narayana., S. Krishnamoorthy, Suja Surendran., M. Chidananda Kumar, Ashwin G.Raj., Advocates, B.G. Nayanatara, CGSC, B.V. Vidyulatha, N.S. Narasimha Swamy, Nalini Venkatesh, Nagaraja Hegde, Somashekar, G. Srinivasan, H.S. Suresh, Shwetha Anand, Pradeep S. Sawkar, K. Rajashekar, C. Manjunath, Advocates, H. Shanthi Bhushan, DSGI, Nandita Haldipur, B.V. Vidyulatha., B. Manjunath, Advocates, P Nishan Unni, CGC, Bheemaiah, V.C. Sudeep, B Venkatanarayan, K. Rajashekhar, Sharaschandra Ramesh Dodawad., CGSCs, B.V. Vidyulatha, V.S. Naik, K.N. Vasuki, B.C. Prabhakar, G. Srinivasan, Ricob Chand, T. Rajaram, Advocates. |

| Date of Judgment : 30-04-2026 |

| Head Note :- |

Constitution of India - Articles 226 & 227 -

|

| Summary :- |

1. Statutes / Acts / Rules / Orders / Regulations Mentioned:

- Articles 226 and 227 of the Constitution of India

- Employees' Provident Funds and Miscellaneous Provisions Act, 1952

- Section 17 of the Employees' Provident Funds and Miscellaneous Provisions Act, 1952

- Section 6 A of the Act, 1952

- Employees' Pension Scheme, 1995

- Paragraph 11(4) of the Scheme, 1995

- Paragraph 11(3) of the Scheme, 1995

- Notification No. GSR 609(E) dated 22‑8‑2014

- Article 142 of the Constitution of India

- Employees' Provident Fund Organisation & Anr. v. Sunil Kumar & Ors (2023) 12 SCC 701

- R.C. Gupta & Ors. Etc. v. Regional Provident Fund Commissioner Employees Provident Fund Organisation & Ors ((2018) 14 SCC 809)

- Annexurec1 to C19 rejection orders Nos. KN/MLR/Higher wages pension /20171/770/2024‑25 dated 06/01/2025

- No. KN/MN/RO/ POHW/KNMLR38967/72/2025‑26 dated 09.04.2025

- Internal circulation/communication dated 18.01.2025

- Impugned order of the Employees Provident Fund Organization dated 27.01.2025

- Annexure‑A bearing No. B4/BNG/RD/MALLESHWARAM/POHW/2418/EX,P/REJ/2025/63

2. Catch Words:

joint option, higher pension, exemption, trust rules, contribution on actual wages, pensionable salary, ceiling wage, time limit, quash, writ of certiorari, Employees’ Provident Fund, Employees’ Pension Scheme, statutory interpretation, financial burden

3. Summary:

The Court examined multiple writ petitions filed under Articles 226 and 227 challenging the rejection of joint‑option applications by the EPFO for higher‑wage pension contributions by members of exempted establishments. The petitioners argued that, based on the Supreme Court judgments in *R.C. Gupta* and *Sunil Kumar*, employees who contributed to the Provident Fund on actual wages are entitled to exercise the joint option under Paragraph 11(3) and 11(4) of the 1995 Pension Scheme, irrespective of the Trust Rules or a pre‑2014 contribution to the pension fund. The respondents contended that the Trust Rules and the 01‑09‑2014 cut‑off barred such exercise. The Court held that the Apex Court’s rulings supersede the Trust Rules, extending the window to exercise the option and directing EPFO to accept the joint options, recalculate pensions on actual wages, and implement the orders within 90 days. The impugned rejection orders were quashed.

4. Conclusion:

Petition Allowed |

| Judgment :- |

|

(Prayer: This Writ Petition is filed under Articles 226 and 227 of the Constitution of India praying to a. quashing the impugned order of the Employees Provident Fund Organization which comes under the Ministry of Labour and Employment, Govt. of India dated 27.01.2025 passed by Asst. Provident Fund Commissioner, Regional Office, Bengaluru, Malleshwaram Inter-Alia rejecting the Joint Options/Applications submitted by the members/pensioners of the BEML Establishment which are hereby held as not eligible at Annx-A bearing No.B4/BNG/RD/MALLESHWARAM/POHW/2418/EX,P/REJ/2025/ 63 and etc.

This Writ Petition is filed under praying to a) to issue a writ of certiorari to quash the Annexurec1 to C19 rejection orders Nos. KN/MLR/Higher wages pension /20171/770/2024-25 dated 06/01/2025 issued to petitioners 1 to 15 and 19 and No.KN/MN/RO/ POHW/KNMLR38967/72/2025-26 dated 09.04.2025 issued to petitioners 16 to 18 by the 3rd Respondent RPFC, EPFO, Mangaluru, by calling for the records leading to the issuance of this order and etc.)

CAV Judgment

1. Two essential questions that arise for consideration in this batch of writ petitions are:

(i) "Are the members of the Provident Fund Trusts of the exempted establishments, who claim to have contributed to the Provident Fund on actual wages (not on capped wages) as per applicable Trust Rules, but contributed to the Pension Fund only on the capped pensionable wages (not on actual wages exceeding the said cap), claim a higher pension under Paragraph 11(4) of the Employees' Pension Scheme, 1995, by exercising a joint option along with the employer, after 01.09.2014?"

(ii) If the provisions of the Trust Rules of the exempted establishments, do not provide for contributions to the pension fund on the actual wages, can the employee who has contributed on the actual wages to the provident fund, claim higher pension?

2. The reliefs sought in the respective petitions are summarised hereunder:

2.1 The petitioners, except in the W.P. No.33271/2025 seek:

(a) To quash the order passed by the Assistant Provident Fund Commissioner rejecting the joint options/applications submitted by the petitioners, opting for higher contribution to the pension on actual wages in excess of caped pensionable wages.

(b) To direct respondents to issue revised pension orders, with interest.

2.2 The petitioners in W.Ps.No.29267/2025, 29408/2025, 29502/2025, 29776/2025, 30785/2025, 32436/2025, 32451/2025, 34464/2025, 34466/2025, 37213/2025, in addition to the prayer mentioned above seek;

(a) To quash the internal circulation/communication dated 18.01.2025 issued by the Provident Fund Organisation to its officers issuing guidelines in calculating the pension.

2.3 The petitioners in W.Ps.No.22068/2025, 32829/2025, 32843/2025, 32887/2025, 38022/2025 in addition to the prayer in paragraph 2.1 referred to above seek;

a) To quash the rejection orders issued on the ground that the employer establishment is an exempted establishment under Section 17 of the Employees' Provident Funds and Miscellaneous Provisions Act, 1952 ('Act, 1952').

b) To process the joint memo filed by the petitioners and to comply with the directions laid down by the Supreme Court in Employees' Provident Fund Organisation & Anr. v. Sunil Kumar B. & Ors (2023) 12 SCC 701.

2.4 The petitioners in W.Ps.No.29502/2025, 29776/2025, 34464/2025 in addition to the prayer in paragraph No.2.1 referred to above also seek;

a) To pay the pension due within 15 days from the date of demand notice.

b) Calculate pension drawn during contributory period of service in span of 60 months from date of exit of membership of pension fund

2.5 The petitioners in W.P. No.33271/2025 seek;

a) To declare petitioners' benefit of higher pension based on actual salary.

b) To direct the respondents to pay higher pension on actual salary.

2.6 The petitioner in W.P.No.15749/2025 in addition to the prayer mentioned in paragraph No.2.1 seeks;

a) Reconsideration of the representation made by the petitioners and accept Joint Option.

3. Though the text and form of the reliefs sought in above referred petitions differ, in substance, the petitioners claim right to exercise joint option to contribute on actual wages to the pension fund and thereby claim higher pension.

4. Certain admitted facts.

4.1 The petitioners are either the associations of the employees of exempted establishments under the Act, 1952, or the employees of the exempted establishments. Some of the individual petitioners have retired post 01.09.2014. Members of the petitioners' association or individual petitioners have not retired before 01.09.2014. In other words, the members of the petitioners' association or individual petitioners were existing members of the Provident Fund Scheme and Pension Scheme as of 01.09.2014.

4.2 The members of the petitioners-associations or individual petitioners referred to above are the members of the Provident Fund Trusts of the respective exempted establishments.

4.3 The employers and employees of these exempted establishments made contributions to the Provident Fund maintained by the respective Trusts of such establishments.

4.4 The employers of these exempted establishments also contributed 8.33% of the pensionable wages (not on actual wages, in excess of pensionable wages), to the Pension Fund.

5. The claim that the employees of the exempted establishments contributed on the actual wages, in excess of capped wages to the provident fund is neither specifically disputed nor admitted by the respondents. However, in none of the impugned orders, the applications to exercise the joint option to contribute/transfer to the pension fund on higher wages, is rejected on the ground that the petitioners have not contributed on higher wages to the provident fund. The applications are rejected on the ground that the provisions of the applicable Trust Rules do not provide for contribution to the pension fund on actual wages.

6. Some of the petitioners have produced the records, submitted to the Provident Fund Commissioner, evidencing higher contributions to the provident fund on higher wages. The petitioners have also submitted the declarations in this behalf which are issued by the Provident Fund Organisation, post judgment in Sunil Kumar (supra). These aspects have not been disputed. Thus, the Court would proceed on the premise that the petitions are filed by the association of employees, where the contribution is made to the Provident Fund on actual wages, and contribution to the pension fund on the ceiling wages.

7. The petitioners contend that, although the members of the petitioners-associations and the individual employee- petitioners intended to contribute to the Pension Fund on their actual salary, such contribution was not permitted by the respondent Provident Fund Organisation, though the higher contribution is made to the Provident Fund. The basis for petitioners' claim.

8. The petitioners' claim for higher pension emanates from two judgments of the Apex Court, namely,

(1) Employees' Provident Fund Organisation & Anr. v. Sunil Kumar & Ors.

(2) R.C. Gupta & Ors. Etc. V. Regional Provident Fund Commissioner Employees Provident Fund Organisation & Ors. ((2018) 14 SCC 809)

9. The learned Senior counsel appearing for the petitioners in some of the matters and the learned counsel appearing for other petitioners would urge that the issue raised in the present petitions are covered in terms of the ratio laid down by the Apex Court in R.C.Gupta and Sunil Kumar (supra).

10. It is also urged that, the respondents could not have rejected the applications exercising joint options on the premise that the Trust rules do not enable contribution on higher wages to the pension fund. It is the submission on behalf of the petitioners that impugned orders are in the teeth of the judgment of the Apex Court in R.C.Gupta and Sunil Kumar (supra).

11. It is urged that in R.C. Gupta (supra), the Apex Court has held that, for the members of the provident fund who have been contributing on higher wages/actual wages, in excess of ceiling wages of Rs.6500/p.m., to the provident fund, there is no outer time limit prescribed, to exercise the joint option, under paragraph 11(3) as it stood before 01.09.2014.

12. Elaborating the submission, it is further urged that, the law in R.C. Gupta (supra), is upheld in Sunil Kumar (supra) and the right to contribute on actual wages to the pension fund, is recognised if contribution is made to provident fund on actual wages, even if members had not opted to exercise the joint option for higher contribution to the pension fund before 01.09.2014, despite amendment of 2014.

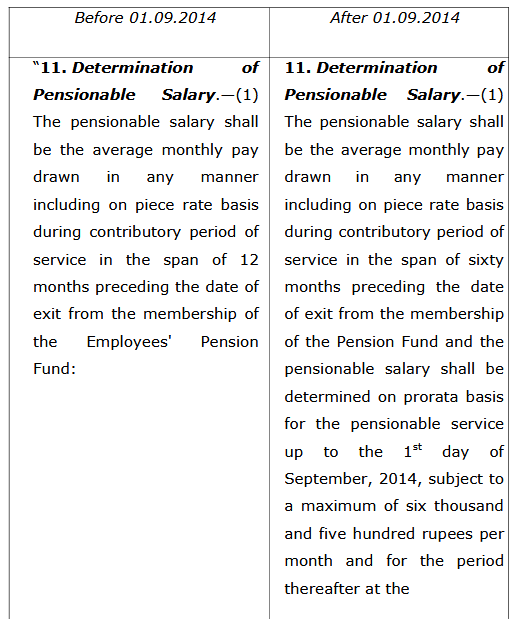

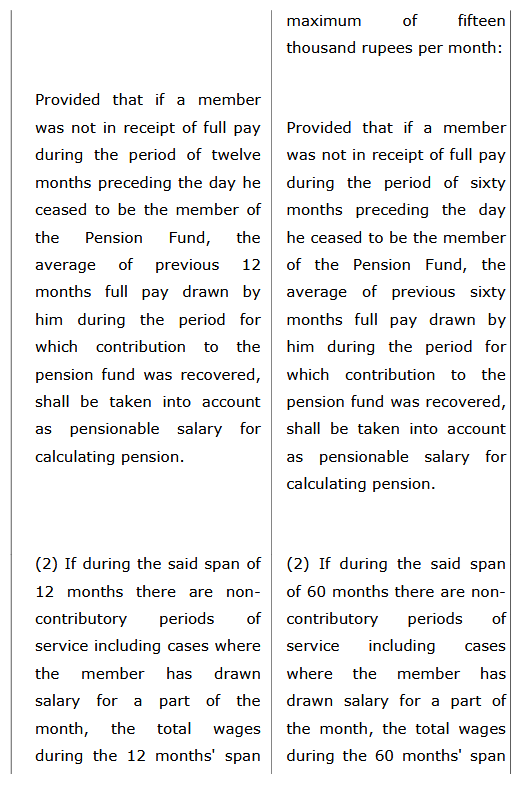

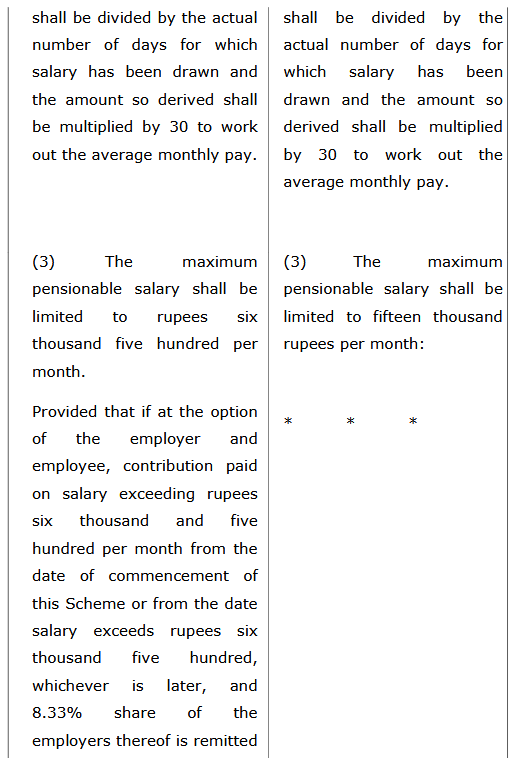

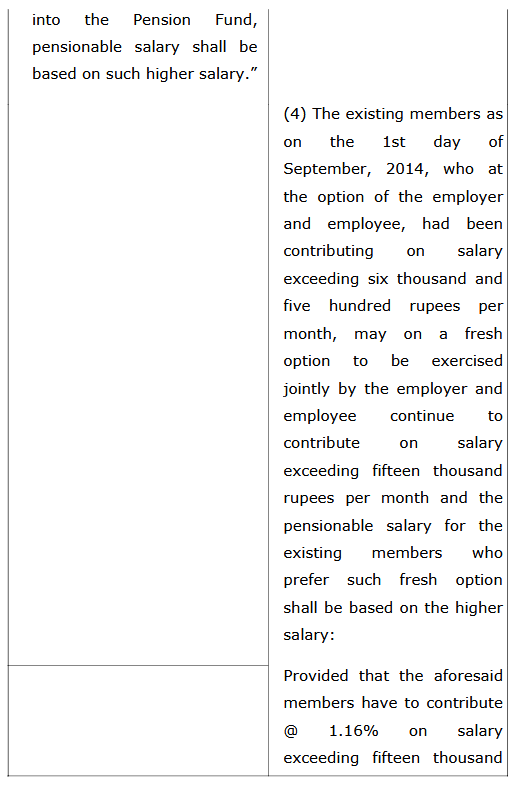

13. Learned counsel appearing for the respondent Provident Fund organisation would refer paragraph 11(4) of the Scheme, 1995. The relevant portion of paragraph 11(4) is extracted hereunder:

11. Determination of Pensionable Salary

xxxxx

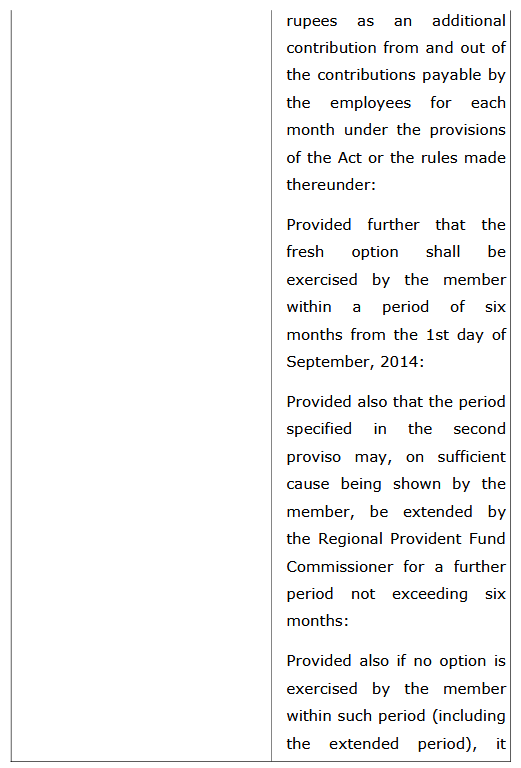

(4) The existing members as on the 1st day of September, 2014, who at the option of the employer and employee, had been contributing on salary exceeding six thousand and five hundred rupees per month, may on a fresh option to be exercised jointly by the employer and employee continue to contribute on salary exceeding fifteen thousand rupees per month and the pensionable salary for the existing members who prefer such fresh option shall be based on the higher salary:

Xxxxx

Provided further that the fresh option shall be exercised by the member within a period of six months from the 1st day of September, 2014:

Provided also that the period specified in the second proviso may, on sufficient cause being shown by the member, be extended by the Regional Provident Fund Commissioner for a further period not exceeding six months:

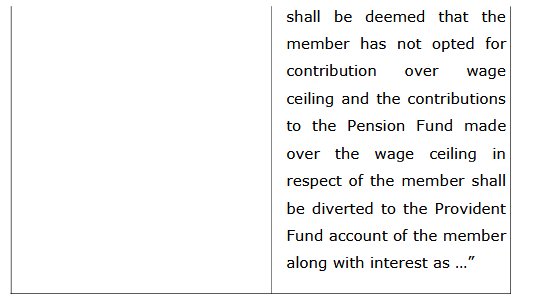

Provided also if no option is exercised by the member within such period (including the extended period), it shall be deemed that the member has not opted for contribution over wage ceiling and the contributions to the Pension Fund made over the wage ceiling in respect of the member shall be diverted to the Provident Fund account of the member along with interest as ..."

(Emphasis supplied)

14. Referring to the above said paragraph No.11(4) of the Pension Scheme,1995, it is urged that the option can be exercised by the existing members who have exercised the option for contributing on higher wages in excess of Rs.6,500/- per month before 01.09.2014. In case the petitioners have contributed on higher wages before 01.09.2014, then only they are eligible to exercise the option for contributing on higher wages to the pension fund is the contention.

15. Elaborating the submissions, learned counsel for the respondents-Provident Fund Organisation urged that, the petitioners admittedly have not contributed to the pension fund on higher wages before 01.09.2014. It is further urged that, the ratio in R.C.Gupta and Sunil Kumar (supra) would come to the aid of the employees who have contributed to the pension fund in excess of the pensionable salary and on the actual salary, before 01.09.2014.

16. In addition, it is urged that the Trust rules of the exempted establishments do not provide for contribution to the pension fund on higher wages/actual wages. And that being the position the petitioners cannot seek the benefit of the law laid down in R.C.Gupta and Sunil Kumar (supra).

17. Learned counsel for the respondent - organisation would also submit that, the excess funds allegedly contributed to the provident fund on the actual wages were not with the organisation and in case the petitioners' claim is allowed, that will impose unmanageable financial obligation on the respondent organisation.

18. The respondent Provident Fund Organisation contends that that eligibility to claim a higher pension is governed by the criteria prescribed under paragraph 11(4) of the Scheme, 1995, as well as the governing Trust Rules of the exempted establishments. In the Trust Rules, applicable to the petitioners there is no provision to contribute on higher wages to the pension fund.

19. Learned counsel for the Union of India, in addition to supporting the submissions made on behalf of the provident fund organisation, would urge that in the event the provident fund organisation is unable to pay the higher pension, then the organisation would seek assistance from Union of India to meet the requirement. It is submitted that the budgetary provisions are not made to meet such a huge outgo and the petitioners claim is untenable.

20. The main objections by the respondents fall under following two categories.

(a) Those provisions of the Trust Rules of the exempted establishments do not provide for contribution on wages exceeding the ceiling limit to the Pension Fund.

(b) That the members of the Fund have not contributed to the Pension Fund on the wages exceeding the prescribed ceiling limit prior to the cut-off date- 01.09.2014, fixed under paragraph 11(4);

21. It is relevant to notice that, the first ground referred to above is found in the impugned orders. The second ground is the reason assigned in the impugned orders, to reject the applications. In few petitions the applications are rejected on the premise, that the applicants are the employees of the exempted establishments. In this background, the present writ petitions have been filed. While most of the petitions raise the aforesaid common issue, a few petitions involve certain additional or distinct questions which are also dealt with in this order.

Background to the Pension Scheme 1995.

22. The Employees' Pension Scheme 1995 (Scheme, 1995) was introduced by the Government of India on 16th November 1995 under the Employees' Provident Funds and Miscellaneous Provisions Act, 1952. The Scheme's statutory source is Section 6 A of the Act, 1952.

23. The paragraph No.3 of the Scheme, 1995 provides for 8.33% contribution to the pension fund by the employer on the pensionable wages/salary. However, the Scheme, 1995 also provides for higher contribution to the pension fund based on the actual salary on exercise of joint option by the employer and employee.

24. For the sake of convenience, the paragraph 11 of the Pension Scheme, 1995 before the 2014 amendment as well as after amendment is reproduced as under:

25. From the above quoted provisions of the Scheme, 1995, it is evident that till the amendment dated 22nd August 2014, which came into effect from 01.09.2014, the Employees had an option to contribute to the Pension Fund on the actual wages, as provided under paragraph 11(3) of the Scheme, 1995. The said paragraph did not stipulate any time limit to exercise the option.

26. Post 01.09.2014, the contribution to the Pension Fund under the Scheme, 1995, is governed by paragraph 11(4), introduced by way of amendment. The proviso to paragraph 11(4) retained the option for higher contribution on actual salary, for the members who were exercising the option for higher pension before 01.09.2014. In addition, the clause also fixed a time frame of six months, extendable by another six months, for sufficient cause to be shown, to exercise the joint option for higher pension.

27. Paragraph 11 of the Scheme, 1995, as amended with effect from 01.09.2014, was the subject matter of challenge before various High Courts, and the Kerala High Court struck down the said provision as unconstitutional. Later, the matter was taken to the Apex Court in Sunil Kumar (supra), and the Apex Court held that only the part of the provision insisting on a 1.16% contribution from the member is invalid, and the rest of the provision is valid.

28. The judgment in Sunil Kumar (supra), also refers to the judgment in R.C. Gupta (supra). The view taken in R.C. Gupta (supra) on the scope of paragraph 11(3) of the Scheme, 1995 is affirmed in Sunil Kumar (supra).

29. Relevant portions of the judgment in paragraphs No.3, 7 and 10 in R.C. Gupta (supra), relevant for the purpose are quoted below for ready reference:

3. The appellant employees on the eve of their retirement i.e. sometime in the year 2005 took the plea that the proviso brought in by the amendment of 1996 was not within their knowledge and, therefore, they may be given the benefit thereof, particularly, when the employer's contribution under the Act has been on actual salary and not on the basis of ceiling limit of either Rs 5000 or Rs 6500 per month, as the case may be. This plea was negatived by the Provident Fund Authority on the ground that the proviso visualised a cut-off date for exercise of option, namely, the date of commencement of Scheme or from the date the salary exceeded the ceiling amount of Rs 5000 or Rs 6500 per month, as may be. As the request of the appellant employees was subsequent to either of the said dates, the same cannot be acceded to.

xxx

7. Reading the proviso, we find that the reference to the date of commencement of the Scheme or the date on which the salary exceeds the ceiling limit are dates from which the option exercised are to be reckoned with for calculation of pensionable salary. The said dates are not cut-off dates to determine the eligibility of the employer-employee to indicate their option under the proviso to Clause 11(3) of the Pension Scheme.xxxxxxxxx. A beneficial scheme, in our considered view, ought not to be allowed to be defeated by reference to a cut-off date, particularly, in a situation where (as in the present case) the employer had deposited 12% of the actual salary and not 12% of the ceiling limit of Rs 5000 or Rs 6500 per month, as the case may be.

xxx

10. The above apart in a situation where the deposit of the employer's share at 12% has been on the actual salary and not the ceiling amount, we do not see how the Provident Fund Commissioner could have been aggrieved to file the LPA before the Division Bench of the High Court.

xxxx.

(Emphasis supplied)

30. The scope of paragraph 11(3) before the amendment of 2014 was under consideration before the Apex Court in R.C. Gupta (supra). The Division Bench of the Himachal Pradesh High Court upheld the contention of the Provident Fund Organisation which denied the right to opt for higher pension on the ground that the date of entry into service, or the date of crossing the pensionable wage limit, whichever is later, is the last date to exercise the option for higher wages under paragraph 11(3) of the Scheme, 1995.

31. The Apex Court in R.C. Gupta (supra), held that no cut-off date is fixed under paragraph No.11(3) to exercise option for contribution on actual/higher wages to the pension fund, and set aside the judgment of the Division Bench of the Himachal Pradesh High Court.

32. The judgment in R.C.Gupta (supra), in effect, opened the window or recognised the window to all the members who had contributed to the Provident Fund on the higher side, in excess of pensionable salary/wages, to exercise the joint option to make higher contribution to the Pension Fund without any time limit, as paragraph 11(3) did not contain any such time limit to exercise the joint option.

33. By the time verdict in R.C. Gupta (supra), was delivered, paragraph 11(4) of the Scheme, 1995, had already been introduced by way of amendment with effect from 01.09.2014. The said amendment was under challenge in various Courts. As already noticed, the said challenge before the Kerala High Court was successful, and later the controversy surrounding paragraph 11(4) was resolved in Sunil Kumar (supra).

34. In Sunil Kumar (supra), except the proviso mandating contribution of 1.16% from members, rest of the provision was upheld.

35. Noticing the confusion and uncertainty in the application of paragraph 11(4) of the Scheme, 1995 (because of the stay order granted on the operation of the provision/order invalidating the provision and the final order of the Apex Court substantially upholding the provision), the Apex Court extended the time frame to exercise the option on the premise that, because of the said orders and the prevailing situation, the employees could not exercise the option, by a further four months from the date of the order, i.e., 04.11.2022.

36. Learned counsel for the respondent provident fund organization, repeatedly urged with vehemence that Paragraph 11(4) of the Scheme, 1995, does not enable members to exercise joint option unless two conditions are fulfilled, namely:

(a) The members must have contributed to the pension fund on higher wages.

(b) The contribution must have been made on or before 01.09.2014.

(c ) The applicable provisions of the Trust Rules of the exempted establishments, do not provide for higher contributions on actual wages, to the pension fund.

37. On a plain reading of the paragraph 11(4), one can say that contribution on actual wages to the provident fund, is a must, before 01.09.2014, to be eligible to exercise the option to contribute on the actual wages to the pension fund. However, the said contention/interpretation emanating from the language of paragraph 11(4) is not available post two judgments of the Apex Court in R.C. Gupta, as well as Sunil Kumar (supra).

38. At this juncture, it is relevant to notice paragraph No. 48 and also the operative portion in Sunil Kumar (supra), which are as under:

"48. The dual option, as is contemplated in Para 11(4) of the Pension Scheme (post the 2014 Amendment), has to be merged into one. In the event the employer and employee jointly opt for coverage beyond the salary limit of Rs 15,000, without giving an earlier option under the unamended Clause 11(3) of the Pension Scheme, they would not be automatically excluded from their right to exercise option under Para 11(4) of the Scheme, post amendment."

39. The relevant operative portion of the judgment in Sunil Kumar (supra) are as under:

" 50. We accordingly hold and direct:

50.1. The provisions contained in Notification No. GSR 609(E) dated 22-8-2014 are legal and valid. So far as present members of the fund are concerned, we have read down certain provisions of the Scheme as applicable in their cases and we shall give our findings and directions on these provisions in the subsequent sub-paragraphs.

50.2. Amendment to the Pension Scheme brought about by Notification No. GSR 609(E) dated 22-8-2014 shall apply to the employees of the exempted establishments in the same manner as the employees of the regular establishments. Transfer of funds from the exempted establishments shall be in the manner as we have already directed.

50.3. The employees who had exercised option under the proviso to Para 11(3) of the 1995 Scheme and continued to be in service as on 1-9- 2014, will be guided by the amended provisions of Para 11(4) of the Pension Scheme.

50.4. The members of the Scheme, who did not exercise option, as contemplated in the proviso to Para 11(3) of the Pension Scheme (as it was before the 2014 Amendment) would be entitled to exercise option under Para 11(4) of the post amendment Scheme. Their right to exercise option before 1-9-2014 stands crystallised in the judgment of this Court in R.C. Gupta [R.C. Gupta v. EPFO, (2018) 14 SCC 809 : (2018) 2 SCC (L&S) 745] . The Scheme as it stood before 1-9- 2014 did not provide for any cut-off date and thus those members shall be entitled to exercise option in terms of Para 11(4) of the Scheme, as it stands at present. Their exercise of option shall be in the nature of joint options covering pre-amended Para 11(3) as also the amended Para 11(4) of the Pension Scheme.

50.5. There was uncertainty as regards validity of the post amendment Scheme, which was quashed by the aforesaid judgments of the three High Courts. Thus, all the employees who did not exercise option but were entitled to do so but could not due to the interpretation on cut-off date by the authorities, ought to be given a further chance to exercise their option. Time to exercise option under Para 11(4) of the Scheme, under these circumstances, shall stand extended by a further period of four months. We are giving this direction in exercise of our jurisdiction under Article 142 of the Constitution of India.

50.6. Rest of the requirements as per the amended provision shall be complied with.

50.7. The employees who had retired prior to 1-9-2014 without exercising any option under Para 11(3) of the pre-amendment Scheme have already exited from the membership thereof. They would not be entitled to the benefit of this judgment.

50.8.xxx.

50.9. xxxx.

50.10. xxx.

50.11. We agree with the view taken by the Division Bench in R.C. Gupta [R.C. Gupta v. EPFO, (2018) 14 SCC 809 : (2018) 2 SCC (L&S) 745] so far as interpretation of the proviso to Para 11(3) (pre-amendment) Pension Scheme is concerned. The fund authorities shall implement the directives contained in the said judgment within a period of eight weeks, subject to our directions contained earlier in this paragraph.

50.12. xxx"

(Emphasis supplied)

40. The paragraphs No.48 and 50.3 and 50.4 in Sunil Kumar (supra), are answers to the contention of the respondents.

41. The language of paragraph 11(4) of the Scheme, 1995, which is not noticed in R.C. Gupta (supra), and which was not under consideration in R.C. Gupta (supra), seems to suggest that such an exercise is not permissible if the higher contribution is not made on pension fund, before 01.09.2014.

42. However, in paragraph No.48 in Sunil Kumar (supra), the Apex Court despite noticing the time limit to exercise the option, under paragraph 11(4) has held as under:

"In the event the employer and employee jointly opt for coverage beyond the salary limit of Rs 15,000/- without giving an earlier option under the unamended Clause 11(3) of the Pension Scheme, they would not be automatically excluded from their right to exercise option under Paragraph No.11(4) of the Scheme, post amendment".

43. In addition to that as already noticed, in paragraph 50.4 in Sunil Kumar (supra), the Apex Court specifically enabled the employers and employees to exercise the joint option under paragraphs 11(3) and 11(4) of the Scheme, 1995 even after 01.09.2014, to contribute on the actual wages to the pension fund, if the employer and employee had contributed on the actual wages to the provident fund.

44. In Sunil Kumar (supra), the Apex Court did not limit the right to exercise the joint option for contributing to the pension fund only to those persons who have contributed before 01.09.2014.

45. It is also relevant to notice in R.C. Gupta (supra), the Apex Court taking note of the way in which the Scheme operates and funds are transferred and operated under the Scheme, has concluded that what is required is adjustment of accounts as higher contribution is already made to the provident fund if not to the pension fund.

46. The conjoint reading of the judgments in R.C. Gupta (supra) and Sunil Kumar (supra) yields the following principles:

(a) The law in R.C. Gupta (supra) (for those who have contributed on higher side to the provident fund) which held that there is no time limit to exercise the joint option under paragraph 11(3), has been affirmed as good law in Sunil Kumar (supra). In other words, the employees who contributed on higher wages to the provident fund are enabled to exercise the option under paragraph 11(3) of the Scheme, 1995, sans any time frame in view of the law declared in R.C. Gupta in 2016.

(b) In Sunil Kumar (supra), the Apex Court expressly held that employees who have contributed on higher side to the provident fund, who had not exercised the option under the unamended Paragraph 11(3) are not precluded from exercising option under Paragraph 11(4) of the Scheme,1995.

(c) The Court further directed that such employees be afforded a fresh opportunity to exercise joint option, and accordingly extended the time limit by four months from 04.11.2022, in exercise of powers under Article 142 of the Constitution.

(d) The right to exercise option, therefore, stands crystallised in favour of eligible employees (those who have contributed on higher side to the provident fund), subject to compliance with the conditions of the Scheme.

47. The contention that only those employees who have contributed on actual wages in excess of the ceiling limit to the Pension Fund are eligible to contribute a higher amount under paragraph No.11(4) of the Scheme, 1995 cannot be accepted for the reasons already noted.

48. The petitioner in R.C. Gupta (supra), did not claim that he contributed on higher wages to the pension fund. The petitioner in the said case claimed that he contributed on higher wages to the provident fund and petitioner's request to exercise the option to claim pension on higher wages was turned down by the Authority under the Scheme. The observations in R.C. Gupta (supra), that;-

"A beneficial scheme, in our considered view, ought not to be allowed to be defeated by reference to a cut-off date, particularly, in a situation where (as in the present case) the employer had deposited 12% of the actual salary and not 12% of the ceiling limit of Rs.5000/- or Rs.6500/- per month, as the case may be" leaves no room for doubt that the employee in that case claimed to exercise the option to make higher contribution to the pension fund belatedly (somewhere in the year 2005), and not immediately on joining service or crossing pensionable wages.

(Emphasis supplied)

49. Apex Court did not say that such an exercise is permissible only for those who are contributing on higher side to both provident and pension fund. The Apex Court expressly allowed exercise of joint option, under paragraphs 11(3) and 11(4) even to those who had not exercised the option for higher contribution to the pension fund under 11(3), provided the employee had contributed on higher wages to the provident fund.

50. The petitioners, in this case, have contributed to the Provident Fund on actual salary in excess of ceiling wages. Therefore, the law in R.C.Gupta (supra), will come to their aid to exercise the joint option, to claim pension on higher salary by exercising the joint option as the Apex Court in R.C. Gupta (supra), has held that there is no time limit to exercise the option and in Sunil Kumar (supra) the Apex Court endorsed the view in R.C. Gupta (supra), and further fixed the time to exercise the joint option.

51. Now the Court has to consider whether the respondents can deny the exercise of joint option to contribute to the pension fund in actual wages on the premise that the Trust Rules, do not enable contribution to the pension fund on higher wages.

52. The contention that the Trust Rules do not provide for contribution on wages exceeding the ceiling cannot, by itself, defeat the statutory right recognised under the Scheme, 1995. The paragraph 39 of the Scheme 1995, which deals with exemption from the Scheme 1995, provides for such exemption from the application of Scheme 1995, only if the other pension scheme to which the employee is a member is on par with the Scheme, 1995 or more favourable to the employee.

53. When the Scheme 1995, provides, under paragraphs 11(3) and 11(4) that the employer and employee are entitled to exercise the joint option, for contribution on actual wages, to the pension fund, in excess of ceiling wages, the respondents cannot deny the right of the employer and employee to exercise the joint option.

54. In addition, both in R.C. Gupta and Sunil Kumar (supra), the Apex Court did not stipulate that the exercise of joint option is permissible for contribution for pension fund on actual salary, only if the Trust Rules provide for such contribution. The Trust Rules even if, does not specifically provide for such contribution to the pension fund, Paragraph No.39 of the Scheme, 1995, comes to the aid of the employees. However, if the authorities under the Scheme,1995, are able to establish that despite insistence to contribute on higher wages, the employee has refused to contribute on higher wages to the pension fund, then conclusion may differ.

55. It is also well settled that in the event of conflict between the Trust Rules and Scheme, 1995, one which is favourable to the employee will prevail. Since the Scheme, 1995 provides for contribution on actual wages to the pension fund, on establishing the contribution to the provident fund, on actual wages, the right will be available to the employee to exercise joint option, subject to any other eligibility criteria. Discussion relating to Exempted Establishments in W.P. Nos 22068/2025, 32829/2025, 32843/2025, 32887/2025, 38022/2025

56. In the aforementioned writ petitions the applications seeking joint option have been rejected on the premise that the petitioners in those petitions were the members of the exempted establishments. It is noticed from the records that the exemption was surrendered in the year 2022.

57. Thus, it is a case of non application of mind by the respondent authorities under the Act, 1952. It is also relevant to notice the Apex Court in paragraph No.50.2 in Sunil Kumar (supra), has expressly held that the amended provisions of the Scheme apply in the same manner as it applies to unexempted establishments.

58. Though it is urged that the petitioners' claim if allowed would result in huge financial burden on the organisation and the Union of India, the Court is of the view that the entitlement of the employees will have to be determined based on the provisions of the Employees' Provident Fund Scheme, 1952 and Employees' Pension Fund Scheme, 1995.

59. If the employees are otherwise entitled to exercise the option under the applicable scheme, such entitlement cannot be curtailed on the premise that it will impose huge financial burden on the organisation.

60. This being the position, the Court is of the view that the applications could not have been rejected in Writ Petitions No. 22068/2025, 32829/2025, 32843/2025, 32887/2025, 38022/2025 on the premise that the petitioners were employees of unexempted establishments. Thus, said impugned orders in those petitions have to be set-aside.

61. CONCLUSION:

In view of the above discussion, it is held:

61.1 Employees who were members of the Employees Pension Scheme, 1995 as on 01.09.2014, in exempted establishments, are entitled to exercise joint option under Paragraph 11(4), even if no option was exercised under Paragraph 11(3) prior to the amendment, provided the contribution was made on actual wages, subject to other applicable eligibility criteria.

61.2 Such option should be exercised within the time limit fixed by the Apex Court in Sunil Kumar (supra) or within such time extended by the Employees Provident Fund Organisation.

61.3 The rejection of application on the ground that no prior contribution was made to the Pension Fund on wages exceeding the ceiling, or that no option was exercised before 01.09.2014, is unsustainable in law, if the contribution was made on higher wages to the provident fund.

61.4 The rejection of the application on the ground that the applicable Trust Rules of the establishment did not provide for contribution to the pension fund is impermissible, except in a situation where employers and employees refused to transfer the funds credited on actual wages in the provident fund to the pension fund.

61.5 The impugned orders are contrary to law declared by the Apex Court in R.C. Gupta and Sunil Kumar supra.

62. Hence the following:

ORDER

1. The Writ Petitions are allowed as indicated below.

2. The rejection of the applications of the members of the petitioner-Associations, to exercise the joint option under paragraphs 11(3) and 11(4) of the Scheme, 1995, on the premise that the employees have not contributed to the pension fund on actual wages, despite contributions on higher wages made to the provident fund, is illegal and the said orders impugned in the petitions are quashed.

3. The members of the petitioner-Associations and the individual petitioners subject to other applicable criteria, are entitled to the benefit of higher pension under the provisions of the Scheme, 1995, as the employees have contributed to the pension fund on actual wages/salary and not on the ceiling wages,

4. The respondent/Employees' Provident Fund Organisation is directed to accept the joint options exercised by the employers and employees in accordance with the law laid down in R C Gupta, and Sunil Kumar (supra), and such time extended by Employees' Provident Fund Organisation and shall recalculate/determine the pension payable on such actual wages/salary as applicable and shall disburse the pension accordingly.

5. The impugned Orders in Writ Petitions No. 22068/2025, 32829/2025, 32843/2025, 32887/2025, 38022/2025 rejecting the applications are quashed, as the Apex Court in Sunil Kumar (supra), has held that the amendment brought by Notification No.GSR 609(E) dated 22.08.2014 applies to both to the employees of the exempted as well as unexempted establishments.

5.1 The respondent/Employees Provident Fund Organisation in Writ Petitions No. 22068/2025, 32829/2025, 32843/2025, 32887/2025, 38022/2025 is directed to reconsider the joint applications of the petitioners and proceed further in terms of law laid down in R C Gupta and Sunil Kumar (supra) and pass appropriate orders.

6. The exercise shall be completed within 90 days from the date of receipt of the copy of the order.

7. It is also made clear that in these petitions, the Court has proceeded to adjudicate the controversy in respect of the employees who were the members of the Employees Provident Fund, and Employees Pension Scheme, employed as of 01.09.2014. This judgment does not deal with the question as to whether similar claim of the members under the Employees' Pension Scheme, retired before 01.09.2014 can be entertained.

|

| |