(Prayer: This Crl.RP is filed u/S.397 r/w 401 Cr.P.C by the advocate for the petitioner praying that this Hon'ble Court may be pleased to set aside the Order dated 07.11.2022 passed by the Learned XXI Additional City Civil and Sessions Judge and Principal Special Judge for CBI Cases, Bengaluru (CCH-4) in Crl.Misc.No.7812/2022 arising out of Spl.C.C.No.18/2017 and consequently allow the revision petition filed by the prosecution U/S.308 of the code.)

CAV Order

1. The following three questions fall for consideration in this Criminal Revision Petition:

(i) Whether the certificate issued by the Public Prosecutor under Section 308(1) of the Code of Criminal Procedure, would result in automatic cancellation/forfeiture of the pardon tendered under Section 306 of the Code?

(ii) Whether examination of the accused turned approver under Section 306(4) of the Code of Criminal Procedure is mandatory in case the pardon is tendered by the Special Court which is competent to take cognizance of the offence and to try the accused?

(iii) Whether the respondents (accused No.3 and 4) have violated the terms and conditions of the pardon?

2. This Criminal Revision Petition is filed assailing the order dated 07.11.2022, passed in Crl.Misc.No.7812/ 2022, by which the petitioner's application under Section 308 of the Code of Criminal Procedure ('Code') to prosecute the respondents of this petition, (the accused No.3 and 4 in RC 6(A)/2016) was rejected.

3. The application under Section 308 of the Code, filed in Spl.C.C.No.18/2017 on the file of the XXI Sessions Judge & Principal Special Judge for CBI Cases, Bengaluru, is numbered as Crl.Misc.No.7812/2022.

4. The petitioner, the Central Bureau of Investigation (CBI for short), filed the aforementioned application to prosecute PW-1 and PW-2 (accused No.3 and 4 turned approvers) for not having complied with the terms and conditions of the order granting pardon.

5. The XVII Additional Chief Metropolitan Magistrate, Bengaluru, on 24.08.2016, had recorded the confession statements of accused No.3 and 4 under Section 164(1) of the Code. The said accused, during the course of the investigation, volunteered to be approvers and sought pardon. On an application under Section 306 of the Code, the Special Judge granted pardon to the said accused, subject to the condition that accused No. 3 and 4 should make a full and true disclosure and depose the truth before the Court.

6. The respondents (who were by then cited as CW-37 and CW-38 in the charge sheet) were examined as PW-1 and PW-2 by the prosecution. Both witnesses were cross-examined by the remaining accused.

7. When the case was posted for final arguments, the Public Prosecutor filed an application under Section 308(1) of the Code to prosecute the respondents, alleging that the approvers had violated the terms of the pardon. The respondents contested the application.

8. The Trial Court framed two points for consideration as follows:

(i) Whether the prosecution establishes that the respondents have not complied with the terms of the pardon?

(ii) What order?

9. The Trial Court, after hearing both sides, dismissed the petition.

10. Initially, the application under Section 308(1) of the Code was not accompanied by a Public Prosecutor's certificate, and the respondents opposed the application on that count. Subsequently, the Public Prosecutor's certificate was filed, and the Trial Court proceeded to hear the matter, holding that the defect is cured. The Trial Court is right in holding that such an omission is curable.

11. The Special Court considered the statements of PW-1 and PW-2 and concluded that the respondents have not violated the terms of the pardon. Hence, the CBI is before this Court assailing the said order.

12. Before going into the merits of the petition, it is necessary to record certain facts:

(a) The prosecution had registered an FIR in R.C.No.06(A)/2016 on 17.03.2016 against one Shri Narasimhaswamy S.G. and Shri N. Sundaram, the Superintendents of Customs at the Import Section of Customs at Bengaluru International Airport. The case was registered for offences under Sections 7, 8, 13(1)(d) read with Section 13(2) of the Prevention of Corruption Act, 1988 (for short 'PC Act') and Section 120B of Indian Penal Code (for short 'IPC').

(b) The prosecution alleged that accused No. 1 and 2, the Customs officials, were demanding and accepting illegal gratification from Clearing House Agents, and accused No. 3 and 4, the employees of two Clearing House Agents, collected the bribe from other agents and paid the same to accused No. 1 and 2 for clearing files for the release of imported goods.

(c) During the investigation, accused No. 3 and 4 (the present respondents) under Section 164(1) of the Code before the XVII Additional Chief Metropolitan Magistrate admitted the accusations.

(d) Accused No.3 and 4 filed applications under Section 306(1) of the Code to be the approvers and sought pardon. The CBI filed a memo supporting the said application to treat accused No.3 and 4 as approvers.

(e) Acting on the application under Section 306(1) of the Code, the Special Judge granted the pardon on the conditions which are extracted below:

"They must make full and true disclosure of the whole of the circumstances within their knowledge relative to the offence and to every other person concerned in the commission of the offences whether as principal or abettor.

Accused no.3 and 4 are also cautioned that if it is disclosed that they have willfully concealed anything essential or giving false evidence and not complied with the condition on which the tender of pardon was tendered and accepted by them or for any other offences of which they appears to have been guilty in connection with the same matter and also for the offence of giving false evidence."

(f) Later in the trial, accused No.3 and 4 were examined as PW-1 and PW-2. In cross-examination, according to the prosecution, the said approvers supported the case of the defense.

(g) In this background, the application under Section 308(1) of the Code was filed to revoke the pardon and the same was dismissed. The said order of dismissal is questioned in this petition.

13. Learned counsel appearing for the petitioner raised the following contentions:

(i) While tendering pardon, conditions were imposed on the accused No.3 and 4 that they should make full and true disclosure of the whole circumstances within their knowledge relative to the offence and the persons concerning the offence, whether as principal or abettor. However, the evidence of PW-1 and PW-2 would demonstrate that the respondents have not complied with the terms and conditions of the pardon;

(ii) The respondents supported the prosecution's version in their statements under Section 164(1) of the Code. However, in cross-examination, they took a 'U-turn' from their statements and supported the case of the defence, and thereby violated the terms and conditions of the pardon;

(iii) The statements in the cross-examination of the respondents are contrary to the statements made under Section 164(1) of the Code; as such, case is made out for revoking pardon under Section 308 of the Code;

(iv) The Trial Court, on a certificate issued by the Public Prosecutor under Section 308(1) of the Code, should have proceeded to hold the trial against the approvers, as the revocation of pardon is automatic upon the issuance of such a certificate by the Public Prosecutor.

14. Learned counsel appearing for the respondents raised the following contentions:

(i) The revocation of pardon is not automatic upon a certificate being filed by the Public Prosecutor. The Court has to hear the approvers before passing orders on a certificate for revocation of pardon;

(ii) In the Section 164(1) statements, examinations-in- chief, and cross-examinations, the respondents narrated the truth as known to them; merely because the statements in cross-examination did not support the prosecution's case, that does not mean that the approvers violated the terms of the pardon;

(iii) In the examinations-in-chief, and cross- examinations, the respondents answered specific questions where there was no scope for further elaboration. In such a situation, if the answers do not tally for any reason, that by itself is not a ground to say pardon conditions were violated;

(iv) It is quite possible that the prosecution's theory itself is false and what is stated in the cross- examination is true; therefore, the prosecution cannot file an application under Section 308 merely because the evidence is not to their liking;

(v) If any explanation was needed after cross- examinations, the petitioner could have re- examined the witnesses, but the prosecution chose not to do so.

15. Learned counsel for the petitioner has relied on the following judgment in support of his contentions: State of Maharashtra vs. Abu Salem Abdul Kayyum Ansari and Others ((2010) 10 SCC 179).

16. Learned counsel for the respondent has relied on the following judgments in support of his contention:

(i) Emperor v. Kothia Navalya Bhil (1906 SCC Online Bom 50)

(ii) Dip Chand v. Emperor 1934 SCC Online Lah 264

(iii) Faguna Kanta Nath v. State of Assam 1959 SCC Online SC 41

(iv) Ex.Sepoy Hardhan Chakrabarty v. Union of India (UOI) and Anr. AIR 1990 SC 1210

(vi) Madan Raj Bhandari v. State of Rajasthan 1970 SCR(1) 688

(vi) B.H. Narashima Rao v. Government of Andhra Pradesh 1999 Supp(4) SC 704

(vii) Rammi Alias Rameshwar vs. State of Madhya Pradesh AIR 1999 SC 3544

(viii) Directorate of Enforcement vs. Rajiv Saxena 2020 SCC OnLine Del 719

17. Section 308(1) of the Code reads as under:

"Where, in regard to a person who has accepted a tender of pardon made under section 306 or section 307, the Public Prosecutor certifies that in his opinion such person has, either by wilfully concealing anything essential or by giving false evidence, not complied with the condition on which the tender was made, such person may be tried for the offence in respect of which the pardon was so tendered or for any other offence of which he appears to have been guilty in connection with the same matter, and also for the offence of giving false evidence:

Provided that such person shall not be tried jointly with any of the other accused:

Provided further that such person shall not be tried for the offence of giving false evidence except with the sanction of the High Court, and nothing contained in section 195 or section 340 shall apply to that offence."

(Emphasis supplied)

18. Section 308(1), which provides for the trial of an approver who violates the terms of the pardon, uses the expression "...may be tried for the offence...". In other words, the Court has the discretion as to whether the approver has to be tried or not. Of course, the discretion is not unfettered or absolute. The Court exercising the discretion has to apply its mind to be prima facie satisfied as to whether a case is made out for revocation of pardon.

19. The reasons are as follows:

(i) The process of tendering and accepting pardon is through a judicial order, which confers a certain concession/relief to the approver. Once the pardon is accepted, he is no longer the accused and is not liable for punishment for the alleged offence. Thus, the pardon which is a judicial order cannot be revoked simply by the issuance of a certificate by the Public Prosecutor. While the Public Prosecutor is enabled to issue a certificate, the pardon cannot be revoked unless the Court forms an opinion on prima facie consideration that there is a violation of conditions.

(ii) If the Court were to take the view that a mere certificate of the public prosecutor is sufficient to revoke pardon, it would have the effect of unilaterally setting aside a judicial order. While the accused is entitled to establish later that he did not violate the terms, the contention that pardon is - 16 - revoked solely on a certificate does not align with the scheme of Sections 306 to 308 of the Code, which aims to secure the best evidence. Unilateral revocation without hearing the approver may dissuade such persons from coming forward to be the approvers, defeating the purpose of Section 306.

(iii) If the Parliament intended revocation to be mandatory on the mere issuance of a certificate without a hearing, it would likely have used the expression "...shall be tried..." instead of "...may be tried..." in Section 308.

20. Thus, this Court is of the view that for the Public Prosecutor to urge for the forfeiture of pardon and a consequent trial, must point out that a prima facie case; at that stage, the approver is also required to be heard. However, the scope of the inquiry is limited to:

(i) Whether the certificate prima facie points out violations of the conditions of the tender of pardon?

(ii) Whether the evidence recorded under Sections 164(1) or 306(4) of the Code, or during trial, "prima facie appear to be" lacking a true and full disclosure of the circumstances relative to the offence, principal or abettor within the person's knowledge?

21. The Delhi High Court in Directorate of Enforcement vs. Rajiv Saxena (2020 SCC OnLine Del 719) held that an application under Section 308 with a certificate, is not tenable if the evidence of the approver has not been recorded under Section 306(4). The High Court upheld the Special Judge's power to judicially review the certificate and reject the prayer for revocation and a trial.

22. Learned counsel for the petitioner urged that the Apex Court in State of Maharashtra vs. Abu Salem (supra) held that pardon stands forfeited on a certificate issued by the Public Prosecutor. The Court has considered said judgment; however, in that case, the Court was not determining if revocation was automatic or if the approver must be heard before proceeding to hold trial against the approver. It held that if the approver suppresses material facts and a certificate is issued, the pardon is lifted, but the specific procedural requirement of hearing the approver was not the primary question in the said case.

On the procedure for hearing an application/ certificate under Section 308 of the Code:

23. The Court does not entirely agree with the procedure adopted by the Trial Court in converting the application under Section 308 into a miscellaneous petition. While forfeiture is not automatic, the elaborate procedure adopted before this Court was uncalled for.

24. The Trial Court registered the application as a separate miscellaneous petition, which is not a legal requirement. Although a person whose pardon is recalled must be tried separately for the main offence, the application/certificate under Section 308 itself does not require a separate trial.

25. On an application under Section 308, the Court is only required to consider the prima facie materials after hearing both sides. After such hearing, if the certificate points out a violation, then it must be accepted and further procedures under Section 308 must follow. If prima facie case is not made out the application is rejected, the accomplice remains a prosecution witness.

Whether the Special Judge is required to examine the accused/approver when the accused accepts the tender:

26. In this case, evidence was recorded by the Metropolitan Magistrate under Section 164(1). It is settled law that if a Magistrate tenders pardon, the examination under Section 306(4) is mandatory before committing the matter.

27. In the instant case, the evidence was recorded on 24.08.2016 under Section 164(1). However, the Magistrate did not tender the pardon. Because the case registered under the Prevention of Corruption Act, the application under Section 306 was filed before the Special Court under the said Act. Under Section 5(2) of the Prevention of Corruption Act read with Section 307 of the Code, the Special Judge has the power to tender pardon on the same conditions.

28. Although respondents argue the Court did not examine the accused under Section 306(4), the Apex Court in Deivendran vs. State of Tamil Nadu (AIR 1998 SC 2821) held such examination is not required if the Court trying the offence tenders pardon after committal. In the instant case, the Court taking cognizance is also the Court empowered to try the case. Thus, Section 307 of the code would apply. The expression "same conditions" in Section 307 refers to Section 306(1) and, not the procedures in the subsequent sub-sections. Thus, the Special Judge was not required to examine the approvers under Section 306(1) of the Code. However, it is to be mentioned that there is no bar under Section 307 of the Code to examine the accused turned approver under Section 306(4) of the Code. The Special Court after tendering the pardon may ask the Magistrate to examine the accused turned approver under Section 306(4) of the Code. Adopting such procedure appears to be a prudent approach.

Whether the evidence on record calls for revocation of pardon and warrants a trial against the approvers.

29. The Court has examined the case with reference to the statements of approvers recorded under Section 164(1), the examinations-in-chief, and the cross- examinations.

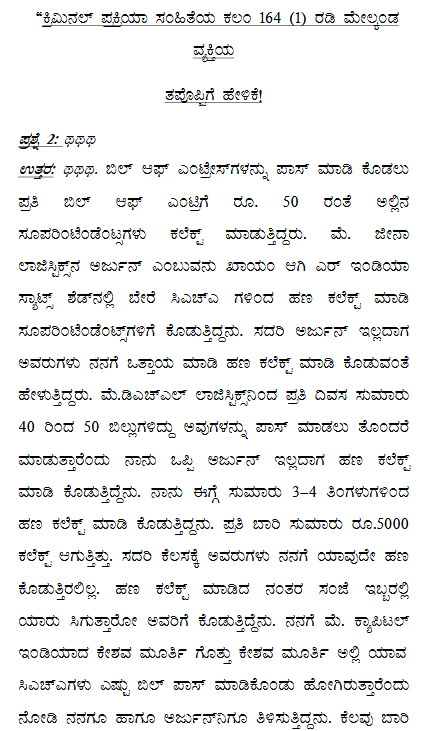

The relevant portion of the evidence of PW-1, Shiva Murthy S.K., under Section 164(1) of the Code, is as under:

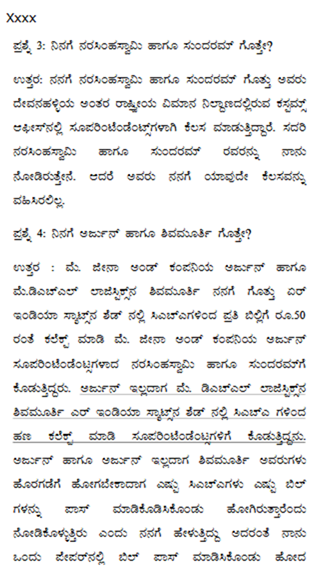

30. In the application under Section 308 (Paragraph No.6), the following statements of Shiva Murthy (Respondent No. 1) are referred to:

"It is true to suggest that CBI Officers have advised me to give a statement to suit this case; as such, I have given the statement as per their say."

"It is also true as I was given an assurance that I will not be shown as an accused and will be set free; therefore, I have not disclosed the said fact to the Magistrate and gave the statement before the Magistrate as per the say of the CBI."

31. In Paragraph No.7 of the said application, the statement of Keshavamurthy (Respondent No. 2) is noted:

"It is true to suggest that CBI officers pressured me to give statement according to their convenience: as such, I have given the statement before the CBI."

"I have not at all collected any amount relating to this case."

32. Referring to the aforementioned statements, it is urged that the conditions of the pardon have been violated.

Respondent No.1, in his statement under Section 164(1), stated that after collecting the amount (from Custom House Agents), he used to give it to Officers of the Customs Department, which is extracted as follows:

33. In paragraph No.5 of the examination-in-chief, PW-1 (respondent No. 1) has stated as under:

"On 14.3.2016, I have collected Rs. 50 per bill of entry from CHAs and in all I collected Rs. 5,000. On the end of the day, I have returned the Rs. 5,000 collected to A1."

34. In the cross-examination, the witness has stated as under:

"20. xxx It is true to suggest that the CBI officers advised me to give a statement to suit this case, as such, I have given the statement as per their say. It is true to suggest that the CBI officers also advised me to get Anticipatory Bail from this court. It is true to suggest that the CBI officers have themselves took me to the Magistrate Court and asked me to give a statement before the Magistrate as required under Sec. 164 of Cr.P.C. It is true to suggest that prior to that I was not at all aware of the location of the said Magistrate Court. It is true to suggest that at the time of recording my statement before the Magistrate Court, the CBI police who took me to the said court were waiting at the door of the said Magistrate Court. It is also true to suggest that before giving the statement, the CBI police gave me my statement and asked me to give the same statement before the Magistrate. It is true to suggest that I have given the statement before the Magistrate like a parrot.

21. xxx I had collected this amount of Rs. 5,000/- on 14.3.2016 and paid it to Sri N. Sundaram and Sri Narasimha Swamy S.G., Superintendents, on their direction. It is true to suggest that CW-11 Arjun was collecting the said amount and he knows much about the collection of the said amount. It is true to suggest that I have not given a statement before the CBI officer naming any particular officer."

35. From the aforementioned statements in the examination-in-chief and the cross-examination, it is evident that PW-1/respondent No. 1 has stuck to his statement that he collected the bribe amount from Custom House Agents and paid it to Customs officials.

36. The relevant portion of the statement under Section 164(1) of the Code, by respondent No.2 (Pw-2, Keshavamurthy P) is as under:

37. The relevant portion of the examination-in- chief of PW2 is extracted as under:

"3. The said Arjun (CW.11) and Shivamurthy (PW.1) used to ask me to do their work, when they used to go for lunch or Tea, during the leisure hour. I used to make the entry of the bills submitted and cleared by the different CHAs in the absence of CW.11 and PW.1.

5. The CW.11 and PW.1 were collecting RS.50 per bill, of entry from the concerned CHAs and they used to deliver the said amount to the Superintendent of Customs."

38. The relevant portion of cross examination of PW2 is extracted hereunder:

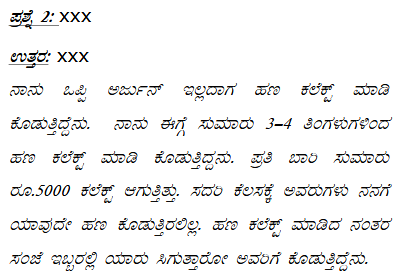

"12. It is true to suggest that I have not at all collected any amount relating to this case M/s Capital Shipping Pvt Ltd., have removed me from their office after 3 days of 16.03.2016. xxx

It is true to suggest that the CBI officer had accompanied me to the Magistrate Court while I was giving statement before the Magistrate. It is true to suggest that at that time, the Magistrate has asked me whether I had accompanied by any police, I answered that no police has accompanied me at that time. It is true to suggest that I have given false statement before the Magistrate. It is not true to suggest that I am giving false evidence to support the accused. It is true to suggest that as I was not having any job and as I was afraid of CBI officer and, my livelihood, I had given the statement before the CBI officer. It is true to suggest that as per the say of CBI officer being afraid of them, I have given the same statement before the Magistrate as a parrot.

14. It is true to suggest that accused were not working the week prior to 14.03.2016 in the said office. It is true to suggest that as I have to save from Job and life, I have given an application for being treated as pardon. It is true to suggest that the CBI officers have assured me that they will let me free if I give the statement as required by them.

15.xxx It is true to suggest that the CW.12 to CW.32 have not at all given me any amount on any day. It is true to suggest that we used to collect amount to help our colleagues who met with an accident or died in an accident. Xxxxx."

39. PW-2/respondent No.2 in his statement under Section 164(1) of the Code has stated that he did not collect the money from Custom House Agents.

40. In the examination-in-chief, both PW-1 and PW- 2 supported the case of the prosecution. PW-1 stated that on 14-03-2016, he collected a sum of ₹5,000 from customs house agents and handed it over to accused No. 1. This version was maintained even in cross-examination.

41. PW-2 in the examination-in-chief and the cross examination has stated that he did not collect any money from customs house agents and did not hand over money to anyone, but that he had maintained records of the number of bills cleared by the Customs officials. He too adhered to this version in cross-examination.

42. From the application under Section 308, it is noticed that the prosecution is contending that respondents have urged that respondents have falsely stated that their statement under Section 164(1) of the Code is not voluntary.

43. It is to be noticed that when the statement under Section 164(1) of the Code was recorded, the application for tendering the pardon had not yet been filed. The Magistrate did not record the statement under Section 164(1) of the Code with a view to tender the pardon. Admittedly, no conditions were imposed while recording the statement under Section 164(1) of the Code.

44. Hence, if the statement under Section 164(1) (which was recorded before the tendering of the pardon) does not disclose all facts concerning the offence or the principal or abettor, it does not amount to a violation of - 32 - the terms and conditions of the pardon, as those conditions were imposed subsequent to the statement under Section 164(1) of the Code.

45. It is to be noticed that pardon was tendered by the Special Judge and not by the Magistrate who recorded the statement under Section 164(1). Moreover, under Section 306(1) of the Code, the accused-turned-approver is required to disclose facts relating to the commission of the offence or facts concerning the principal or abettor. The prosecution is complaining about a subsequent event, viz., the alleged false statement regarding the pressure or inducement by the CBI officials to confess to the commission of the offence.

46. In the cross-examination, Pw1 and Pw2 for the first time revealed that they gave confessional statement under Section 164(1) of the Code at the instance of the CBI officials. The question is whether the said statements made in the cross-examination can be termed as a violation of the terms and conditions of the pardon.

47. The Court is of the view that the said statements in the cross-examination, that the CBI officials pressurized or induced accused No.3 and 4 to make a confessional statements under Section 164(1) of the Code, even if true, cannot be termed as violation of the terms of the pardon. The reason is that, if the said statements are true, then the accused/approvers have narrated the truth and cannot be penalized for it.

48. In the event that such inducement or pressure was not there for making the confessional statement, then evidence in the cross-examination that accused were pressurized and induced to confess under Section 164(1) of the Code may amount to false evidence. If the approver is to be tried for giving false evidence, then the prosecution must seek the leave of the High Court as provided under the proviso to Section 308(1) of the Code. Admittedly, the petitioner has not sought such leave.

49. Thus, on reconsideration of the evidence and the statement before the Court, the Court is of the view that the Pw1/respondent No.1 has stuck to the statement made under Section 164(1) of the Code and in the examination-in-chief when it comes to the facts relating to collecting money and paying the same to the Customs Officials.

50. Likewise, PW.2 in his cross examination has stuck to the stand that he used to count and make notes of the bills cleared and used to hand it over to PW.1. PW.2 has maintained the same stand that he has not collected the amount and paid to the Customs Officials.

51. This being the position, in the facts and circumstances of this case, merely because the approvers did not disclose about the alleged inducement or pressure by the officials to give a statement under Section 164(1) of the Code does not amount to violation of the terms of the pardon.

52. New facts revealed in the cross-examination, ipso facto may not amount to violation of the terms of the pardon. The cross-examination is not just confined to the facts which are testified in the examination-in-chief but also, extend to the facts which are relevant for adjudication. It is apparent from the provision which reads as under:

Section 138 of The Indian Evidence Act, 1872 is extracted as under:

"138.Order of examinations.- Witnesses shall be first examined-in-chief, then (if the adverse party so desires) cross-examined, then (if the party calling him so desires) re-examined.

The examination and cross-examination must relate to relevant facts, but the cross-examination need not be confined to the facts to which the witness testified on his examination-in-chief.

Direction of re-examination.-The re-examination shall be directed to the explanation of matters referred to in cross-examination; and, if new matter is, by permission of the Court, introduced in re-examination, the adverse party may further cross-examine upon that matter."

(Emphasis supplied)

53. In view of the wide scope of cross-examination, every new statement made in the cross-examination by the approver cannot be termed as violation of the terms and conditions of the pardon. Whether, such new statements made in the cross-examination amount to violation of the terms of the pardon depends upon the facts of each case.

54. As rightly urged by the learned counsel for the respondents, on the new facts which are revealed in the cross-examination, the prosecution has not sought re- examination. The learned counsel for the respondent has placed reliance on the judgment of the Apex Court in Rammi Alias Rameshwar (supra), where it is held that re-examination under Section 138 of the Indian Evidence Act, 1872 is not confined to clarification of ambiguities in the cross-examination. The observations in paragraphs No.16 and 17 of the said judgment are relevant and extracted hereunder:

"16. The very purpose of re-examination is to explain matters which have been brought down in cross-examination. Section 138 of the Evidence Act outlines the amplitude of re-examination. It reads thus:

"138. * * *

Direction of re-examination.- The re- examination shall be directed to the explanation of matters referred to in cross-examination; and if new matter is, by permission of the Court, introduced in re-examination, the adverse party may further cross-examine upon that matter."

17. There is an erroneous impression that re-examination should be confined to clarification of ambiguities which have been brought down in cross-examination. No doubt, ambiguities can be resolved through re-examination. But that is not the only function of the re-examiner. If the party who called the witness feels that explanation is required for any matter referred to in cross- examination he has the liberty to put any question in re-examination to get the explanation. The Public Prosecutor should formulate his questions for that purpose. Explanation may be required either when ambiguity remains regarding any answer elicited during cross-examination or even - 38 - otherwise. If the Public Prosecutor feels that certain answers require more elucidation from the witness he has the freedom and the right to put such questions as he deems necessary for that purpose, subject of course to the control of the court in accordance with the other provisions. But the court cannot direct him to confine his questions to ambiguities alone which arose in cross- examination."

(Emphasis supplied)

55. The prosecution could have re-examined the approvers on the new facts narrated in the cross- examination. That is not done.

56. The Court has also noticed the answer to the question put by the learned Special Judge who asked PW.1 as to whether there was any difficulty in disclosing the fact that the CBI Police was waiting at the door while recording statement before the Magistrate. To the said question, the witness has answered stating that he had no such difficulty to disclose the fact.

57. As already noticed, the terms of the pardon were not negotiated and accepted when said statement was made before the Magistrate. Hence, the contention that suppression of alleged pressure or inducement by the police while recording Section 164 (1) statement does not amount to violation of the conditions of the pardon.

58. And as already discussed, the statement relating to pressure and inducement by the CBI officials if is a false statement, then, to prosecute for such false evidence, the prosecuting agency has to seek leave of the High Court which admittedly, is not sought.

59. Before parting, the Court must place on record the valuable assistance rendered by the learned Counsel for both sides.

60. Hence the following:

ORDER

(i) Petition is dismissed.

(ii) Since, the petitioner has not sought the leave of the Court to prosecute the approvers on the premise that approvers have given false evidence; the liberty is reserved to the prosecution to file such petition as advised in law.

(iii) It is made clear that this Court has not expressed any opinion as to whether the statements made by the approvers are false or not. Such question has to be decided on an application, if any, filed seeking leave to prosecute the approvers for giving false evidence.

|

This Product is Licensed to , |