Common Judgment:

1. Both these appeals are directed against the order dated 17.06.2015 passed by the learned Single Judge dismissing WP(MD)No.9411 of 2011 filed by the appellants in WA(MD)No.761 of 2015. The appellant association in WA(MD)No.765 of 2015 got itself impleaded as the seventh respondent in the writ petition vide order dated 04.12.2014.

2. The case on hand pertains to the pension scheme applicable to the retired employees of Oriental Insurance Company Limited, United India Insurance Company Limited, New India Assurance Company Limited and National Insurance Company Limited. The Central Government in exercise of the power conferred by Section 17A of the General Insurance Business (Nationalization) Act, 1972 made applicable the General Insurance (Employees') Pension Scheme, 1995 with effect from 01.11.1993. It was to apply to those in service in the said insurance companies as on 01.01.1986. Clause 2(d) and Clause 34 of the pension scheme read as follows :

“2(d) 'average emoluments' means the average of pay drawn by an employee during the last ten months of his service”

34.Amount of Pension –

(1) In respect of employees who retired between the 1st day of January, 1986 but before the 31st day of July, 1987, basic pension and additional pension will be updated as per the formula given in Appendix-III.

(2) In the case of an employee retiring in accordance with the provisions of the relevant rationalisation scheme after completing the qualifying service of not less than thirty three years, the amount of basic pension shall be calculated at fifty per cent of the average emoluments.

(3) (a) Additional pension shall be fifty per cent of the allowances drawn by an employee during the last ten months of his service. (b) No dearness relief shall be paid on the amount of additional pension.

Explanation:- For the purposes of this sub-paragraph "allowances" means allowances which are admissible to the extent counted for the following purpose only, namely :-

(i) making contributions to the Provident Fund ;

(ii) grant of house rent allowances ;

(iii) payment of gratuity ; and

(iv) re-fixation of salary on promotion.

(4) Pension as computed being the aggregate of subparagraphs (2) and (3) above shall be subject to the minimum pension as specified in this scheme.

(5) An employee who has commuted the admissible portion of his pension as per the provisions of paragraph 40 of this scheme shall receive only the balance of pension, monthly.

(6) (a) In the case of an employee retiring before completing a qualifying service of thirty- three years, but after completing a qualifying service of ten years, the amount of pension shall be proportionate to the amount of pension admissible under subparagraphs (2) and (3) and in no case the amount of pension shall be less than the amount of minimum pension specified in this scheme.

(b) Notwithstanding anything contained in this scheme, the amount of invalid pension shall not be less than the ordinary rate of family pension which would have been payable to his family in the event of his death while in service.

(7) The amount of pension finally determined under this paragraph shall be expressed in whole rupee and where the pension contains a fraction of a rupee, it shall be rounded off to the next higher rupee.

(8) Notwithstanding anything contained in this Scheme, in relation to an employee covered by the proviso to clause (k) of Paragraph 2, pension shall be calculated in accordance with the provisions of sub-paragraph (2), so however, that such pension shall not be less than what he would have been entitled to had he continued in the scale of pay of General Manager, when the pension becomes due and payable to him.”

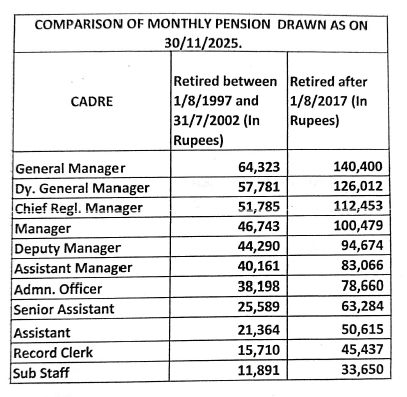

The pay scales of the employees are revised periodically. Such revisions took place during 1989, 1997, 2002, 2007, 2012 and 2017. Since as per Clause 34, the basic pension receivable by a retired employee is pegged at 50% of the average emolument, it tends to be static. The periodical pay scale revisions are not taken note of while calculating the basic pension. As a result, those who retired prior in point of time, though from a higher cadre, draw less pension compared to those who retire from a far lower cadre. This is illustrated by the following comparative chart :

3. A similar situation obtained in the case of the Central Government pensioners also. That was set right by the Government of India vide Notification dated 17.12.1998. It was directed that the pension of all pensioners irrespective of their date of retirement shall not be less than 50% of the minimum pay in the revised scale of pay introduced with effect from 01.01.1996 of the post last held by the pensioners. When the 6th Central Pay Commission Recommendations were implemented, the Government of India vide Office Memorandum dated 01.09.2008, directed that the fixation of pension will be subject to the provision that the revised pension, in no case, shall be lower than fifty percent of the minimum of the pay in the pay band plus the grade pay corresponding to the pre-revised pay scale from which the pensioner had retired. The Tamil Nadu Electricity Board also issued similar Board Proceedings dated 01.12.2009. Thus, the basic pension receivable by a pensioner was quantified based on the revised pay fixed for the post which was held by the pensioner when he retired. This was a beneficial measure introduced by the Central Government for its pensioners. Many other organizations followed suit. However, in the case of the respondent insurance companies, similar change in the pension scheme was not brought about. Though the appellant association and the pensioners represented to the Central Government in this regard, no response was forthcoming. Hence, WP(MD)No.9411 of 2011 was filed for directing the Ministry of Finance, Government of India to grant revised pension and other benefits on the basis of revised pay scale as amended and effected from time to time and to pay all consequential benefits including pensionary arrears. The writ petition however suffered dismissal. Hence, these writ appeals came to be filed.

4. The learned counsel for the appellants submitted that the learned Single Judge erred in not granting relief. He drew our attention to Clause 55 of the pension scheme and contended that the pensioners of the aforesaid insurance companies are entitled to revision of their basic pension on par with the methodology adopted by the Government of India. He pointed out that unless such a change is brought about, the iniquitous position demonstrated by the comparative chart cannot be set right. A person who retired from a higher grade is entitled to receive higher pension compared to a person who retired from a lower grade. This proposition is a natural corollary of the equality principle enshrined in Article 14 of the Constitution of India. Pensioners form a homogenous class and a liberal approach adopted in case of a section has to be applied across the board. The insurance companies in question are possessed of a huge corpus of pension fund and they are in a position to meet any liability that may arise as a result of issuance of a writ of mandamus as prayed for. The learned counsel contended that the learned Single Judge had misapplied the decisions reported in (1990) 4 SCC 207 (Krishena Kumar v. UOI) and (1997) 7 SCC 334 (UOI v. Lieut.Mrs. E.IACATS). The learned counsel relied on the following case laws :

1. D.S. Nakara v. Union of India, (1983) 1 SCC 305

2. R.L. Marwaha v. Union of India, (1987) 4 SCC 31

3. Bharat Petroleum Management Staff Pensioners v. Bharat Petroleum Corpn. Ltd., (1988) 3 SCC 32

4. All India Reserve Bank Retired Officers Assn. v. Union of India, 1992 Supp (1) SCC 664

5. V. Kasturi v. Managing Director, State Bank of India, (1998) 8 SCC 30

6. Subrata Sen v. Union of India, (2001) 8 SCC 71 AND

7. All Manipur Pensioners Assn. v. State of Manipur, (2020) 14 SCC 625.

The learned counsel filed written submissions and took us through the same. He called upon us to set aside the order of the learned Single Judge and allow the writ appeals.

5. Per contra, the learned counsel appearing for the respondents submitted that the order of the learned Single Judge is well reasoned and that it does not call for interference. Shri.V.Perumal, the learned counsel appearing for the insurance companies also filed detailed written arguments and took us through its contents. He raised prelimnary objection as regards the maintainability of these writ appeals at the instance of the Appellant Association.

6. We carefully considered the rival contentions and went through the materials on record. The objection of the respondents that the writ appeal filed by the association has to be dismissed as not maintainable is without substance. While a writ petition by an association could possibly be contested on grounds of maintainability, an appeal by an association which was a party to the writ proceedings is obviously maintainable. It is well settled that any aggrieved person can file a writ appeal under Clause 15 of the Letters Patent. If an association felt aggrieved by the order of the learned Single Judge, it can definitely maintain an appeal. It would be all the more so when it is a party to the writ petition itself. An association has no fundamental right and therefore, it cannot maintain a writ petition under Article 32 of the Constitution of India (vide Mohinder Kumar Gupta v. UOI (1995) 1 SCC 85). But a writ petition filed under Article 226 of the Constitution can be maintained for enforcing a statutory right or for any other purpose. A writ petitioner need not demonstrate the existence of any fundamental right. It is enough that there is locus standi. The appellant-association would definitely pass muster on that count. The appeal has been filed to espouse the cause of the members of the association. The Hon'ble Supreme Court in the decision reported in (1983) 1 SCC 305 (D.S.Nakara v. UOI) upheld the locus standi of a registered society to take up the cause of its members by seeking remedy through judicial process. The same approach was adopted by the Hon'ble Supreme Court in Confederation of Ex.Servicemen Associations v. UOI (2006) 8 SCC 399. The Division Bench of the Madras High Court in the decision reported in (2006) 2 CTC 705 (Vellakoil Vattara Vari Seluthuvor Nalvalvu Sangam v. State of T.N) held that writ petition filed by a registered society for the benefit of its members is very much maintainable. When a registered association can maintain a writ petition, it can obviously maintain a writ appeal also.

7. Right to receive pension is recognised as a right in property (State Of Jharkhand & Ors. vs Jitendra Kumar Srivastava & Anr (2013) 12 SCC 210). Right to receive pension, although accruing on retirement, is a condition of service (UOI v. Gurnam Singh, (1982) 2 SCC 314). The Constitution Bench of the Hon'ble Supreme Court in the decision reported in (1971) 2 SCC 330 (Deokinandan Prasad v. State of Bihar) declared that pension is not a bounty payable on the sweet will and pleasure of the government but is a valuable right vesting in a government servant. But then, payment of pension would only be as per the rules (Union of India v. Satish Kumar, (2006) 1 SCC 360). The argument of the appellants is not that they are not being paid as per the provisions set out in the General Insurance (Employees') Pension Scheme, 1995. The demand in these proceedings is that the basic pension receivable by a retired employee should not be static but dynamic. It is true that the Central Government has introduced a dynamic element in the pension scheme applicable to the central government pensioners. But the pension scheme applicable to the retired employees of the aforesaid insurance companies does not contain a comparable provision. Unfortunately, the appellants have also not challenged the validity of the 1995 pension scheme. So long as Clauses 2(d) and 34 of the pension scheme remain as they are, the appellants cannot seek anything more than what Clause 34 envisages.

8. Right to receive pension is not a fundamental or a constitutional right. It is governed by statute or regulated by contract. Till the 1995 scheme was introduced by the Central Government, the retired employees of the aforesaid insurance companies did not receive any pension. Their right to receive pension, therefore, stems and flows out of the provisions of the scheme. So long as the scheme provisions remain what they are, the pension quantification also has to be determined only by them. It is true that the Central Government has introduced a liberalised pension scheme for the central government pensioners. Whether to bring the pensioners of the aforesaid insurance companies also on par with the central government pensioners is a policy decision that has to be taken by the central government. It is well settled that the Court cannot compel the Government to formulate a policy, evaluate alternatives or assess the effectiveness of existing policies. This constraint stems from the principle of separation of powers, where the Court lacks the democratic mandate and institutional expertise to delve into such matters. Thus, while the Court can invalidate a policy, it lacks the authority to create one. (vide Citizenship Act, 1955, Section 6-A, In re, (2024) 16 SCC 105). The writ court cannot dictate what the pension policy has to be. This is because it has huge financial implications. The pockets of the insurance companies may be deep. But that is no ground to direct them to cough up more than what they are due and liable. Liability in such matters will have to be determined only in terms of the applicable provisions. While they can be liberally interpreted in pension matters, the court will not be justified in issuing directions contrary to rules (vide V.Sukumaran v. State of Kerala, (2020) 8 SCC 106).

9. The core contention of the appellants is that they are entitled to relief by applying the residuary clause set out in Clause 55 of the pension scheme. It reads as follows :

“Residuary provisions – Matters relating to pension and other benefits in respect of which no express provision has been made in this scheme shall be governed by the corresponding provisions contained in the Central Civil Services (Pension) Rules, 1972 or the Central Civil Services (Commutation of Pension) Rules,1981, applicable for Central Government employees.”

It is a cardinal principle of interpretation of a statute that only those cases or situations can be covered under a residual head which are not covered under a specific head. In other words, what can be brought under a residual provision should not be covered under the provisions preceding it (UOI v. Rajpal Singh (2009) 1 SCC 216). When the amount of pension payable to a retired employee is already covered under Clause 34/35 of the pension scheme, Clause 55, which is a residuary clause, cannot be invoked at all. A residual clause can be pressed into service only in the absence of a provision. Where the field is expressly covered, the residual clause will not kick in.

10. Appeal to Nakara principle or Article 14 of the Constitution of India is equally in vain. Pensioners, no doubt, constitute a genus. But within this overarching circle, there are numerous species. Each would form a sub-circle. A member of one sub-circle cannot seek to compare himself or herself with a member of another sub-circle merely on the ground that they belong to the same genus of pensioners. The claimant must show that he is equally placed in every respect to enforce the mandate of equality. The insurance company in question might be a Government of India Undertaking. But on that score, an insurance employee will not become a central government employee. If that be so, we fail to understand as to how the pensioner of such an insurance company can claim parity with a central government pensioner.

11. The comparative chart shown by the learned counsel for the appellant no doubt appeal to us at the first blush. But this submission is again without any legal force. A Senior Assistant who retired between 01.08.1997 and 31.07.2002 would get monthly basic pension of Rs.25,589/- but a sub-staff who retired after 01.08.2017 would get Rs.33,650/-. This looks anomalous. But there is actually no anomaly. No generation should compare itself with its succeeding generation. They belong to different time-zones. The basic pension is fixed on the basis of the last drawn pay. Due to rise in prices, increase in cost of living and other inflationary factors, pay scales are periodically revised. Therefore, a sub-staff who joins the post a decade later would obviously be getting a higher pay compared to those who occupied higher grades earlier. It is said that comparisons are always odious. This proverbial wisdom is of apposite application in this case. Those who retire later get higher pension because their last drawn pay was higher. In other words, their drawing higher pension is not on account of any application of a different formula. The very same provision that applies to a Senior Assistant who retired between 1997 and 2002 has been applied to the sub-staff who retired after 2017. Thus, there is no infraction of the equality principle. One cannot infer anomaly merely because of the drawal of higher pension by a person belonging to a lower cadre without taking note of when he retired.

12. We fully concur with the reasons assigned by the learned Single Judge. We, therefore, refrain from extensively quoting the case laws relied on by the learned Single Judge.

13. We should not however be understood as holding that the demand of the appellants is unreasonable. Far from it. However, it is a matter to be benevolently considered by the Central Government. The managements of the respondent insurance companies might as well take up the matter. The petitioners can very well pursue the matter with the governmental authorities. The dismissal of these writ appeals will not and ought not to discourage them from pursuing the matter. Since the hands of the writ court are tied and the issue involves policy implications, we decline to interfere.

14. With the aforesaid observations, these writ appeals are dismissed. No costs. Connected miscellaneous petitions are closed.

|

This Product is Licensed to , |