Case No : Writ Petition No. 18122 Of 2025 (GM-DRT)

Judges: THE HONOURABLE MRS. JUSTICE LALITHA KANNEGANTI

Parties : Ganjam Nagappa & Son Private Limited, Through Authorised Representative, Ganjam Bimaji Umesh, Karnataka Versus Reserve Bank Of India, Through Its Regional Director Regional Office, Bengaluru & Others

Appearing Advocates : For the Petitioner: Krishnendu Datta Seni, Senior Advocate, C. Manjunath, Advocate. For the Respondents: R1, B.T. Manik, Advocate, R2, Thimmanna Bhat, CGC, G.C. Mahabaleshwar, Advocate, R4, Vikram Huilgol, Senior Advocate, Lakshmi K. Valdalag, R5, Vignesh Shetty, R6, Francis Xavier, Advocates, R7, C.K. Nandakumar, Senior Advocate, Raghuram Cadambi, Advocate.

Date of Judgment : 25-06-2026

Head Note :-

Constitution of India - Articles 226 & 227 -

Comparative Citation:

2026 KHC 31655,

Judgment :-

(Prayer: This Writ Petition is filed under Articles 226 and 227 of the Constitution of India, praying to directing the Respondent No. 3 to 7 to comply with the Prudential Framework dated June 7, 2019 (Annexure- H) and convene a review meeting of 30 days of all lenders Respondent No. 3 to 7 such that a joint decision can be taken with respect to resolution/settlement (including latest 2025 OTS Proposal Annexure -B) with respect to debt of the petitioner, and consequently quash and set aside impugned demand notices dated May 2, 2024 and November 30, 2022 (Annexure -C and D) and all subsequent recovery actions against the petitioner, security providers and the secured assets.)

CAV Judgment

1. The present writ petition is filed seeking the following prayer:

"PRAYER

THEREFORE, in light of the facts and circumstances presented herein, it is most humbly prayed before this Hon'ble High Court that this Hon'ble High Court may be pleased to:

(a) Issue a writ in the nature of Mandamus or any other appropriate writ directing the Respondent No. 3 to 7 to comply with the Prudential Framework dated June 7, 2019 (Annexure H) and convene a review meeting of 30 days of all lenders - Respondent No. 3 to 7 such that a joint decision can be taken with respect to resolution/settlement (including latest 2025 OTS Proposal - Annexure B) with respect to debt of the Petitioner, and consequently quash and set aside Impugned Demand Notices dated May 2, 2024 and November 30, 2022 (Annexure C and D) and all subsequent recovery actions against the Petitioner, security providers and the secured assets;

(b) Issue a writ in the nature of certiorari or any other appropriate writ declaring that the classification of debt of Petitioner by the Respondent No. 4 (acting for Respondent No. 4 to 7) is illegal and non-est on the ground that accounts of Petitioner were regularized on February 8, 2024 (Annexure AA) and minimum 90 days period as per IRAC Norms dated April 2, 2024 (Annexure CC) was not expired on April 30, 2024, and consequently declare illegal, quash and set aside the Impugned Demand Notice dated May 2, 2024 (Annexure C) issued by the Respondent No. 4 declaring the accounts of Petitioner as non-performing assets as of April 30, 2024 and all subsequent recovery actions against the Petitioner, security providers and the secured assets;

or in the Alternative of (a) and (b) above,

Issue a writ in the nature of Mandamus or any other appropriate writ directing Reserve Bank of India/Respondent No. 1 to consider and rule on the representation dated April 19, 2025 (Annexure E) made by the Petitioner in relation to the non-compliances by the Respondent No. 3 to 7;

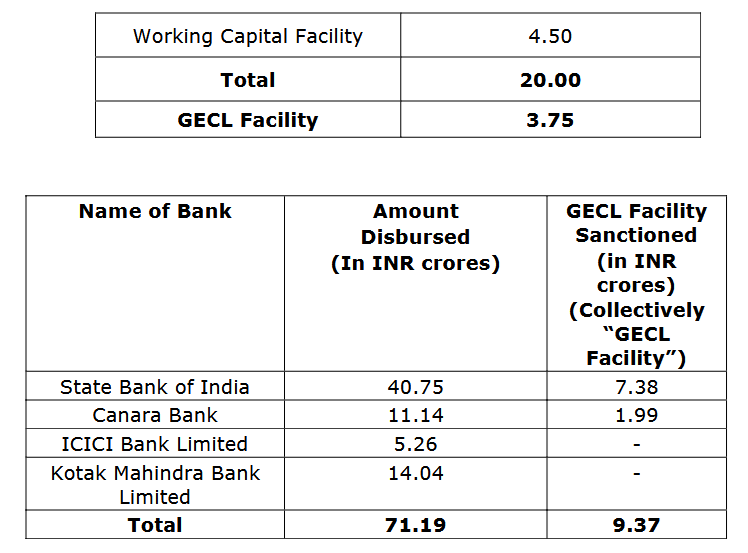

c) Issue a writ in the nature of Mandamus or any other appropriate writ directing Respondent No. 3 to 5 to comply with Emergency Credit Line Guarantee Scheme (ECLGS) issued on May 23, (as supplemented, extended and modified from time to time including on June 29, 2023) and Press Release dated August 5, 2021 (Annexure P and Q), and accordingly, disburse the ECLGS loan amount to the tune of INR 3.75 Crore, INR 7.38 Crore and INR 1.99 Crore respectively to the account of the Petitioner to be exclusively used as per the objective mentioned in the ECLGS Scheme;

or in the Alternative of (c) above,

Issue a writ in the nature of Mandamus or any other appropriate writ directing Respondent No. 2/Ministry of Finance to consider and rule on the representation dated April 21, 2025 (Annexure F) made by the Petitioner in relation to the noncompliances by the Respondent No. 3 to 5 of the ECLGS Scheme (Annexure P);"

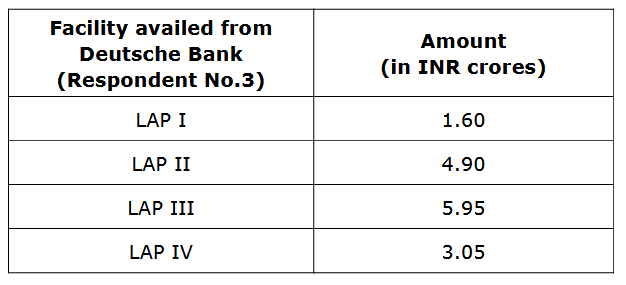

2. The petitioner is a company incorporated under the provisions of the Companies Act, 1956, and is engaged in the business of retailing luxury jewellery and stones. During the period 2016-2021, the petitioner availed the following loans from respondent Nos. 3 to 7:

3. It is stated that in June 2020, as was the case with every borrower and micro, small and medium enterprise in the country, the petitioner faced stress and succumbed to the economic fallout on account of COVID-19. Despite the financial difficulties faced by the petitioner due to the impact of COVID- 19 and the moratorium provided by Respondent No. 3 on the payment of principal and interest for the period from March 1, 2020, to May 31, 2020, the petitioner was forced to utilise the funds to service its debt from the minimal revenue generated, instead of revamping its business. Owing to the continuing stress, the petitioner requested the lenders for restructuring on various occasions, and accordingly, the Consortium Lenders commenced their review. In view of the above, the petitioner requested Respondent No. 3 to join the Consortium Lenders in order to arrive at a decision as to whether or not to proceed with the restructuring of the petitioner's account. However, Respondent No. 3, as recorded in the minutes of the meeting dated December 28, 2020, did not attend the meeting due to short notice and other commitments.

4. It is stated that the Consortium Lenders had principally agreed to restructuring, though they could not agree to a particular restructuring plan during that meeting and accordingly postponed the same for subsequent meetings. Respondent No. 2 issued the ECLGS Scheme through the National Credit Guarantee Trustee Company Limited to provide support to businesses to cope with the economic fallout caused by COVID-19. To cope with the economic fallout due to COVID- 19, the Petitioner requested the lenders to extend the GECL facility in accordance with the ECLGS Scheme. Respondents No. 3 to 5 sanctioned the GECL facility. However, instead of disbursing the GECL facility into a separate account of the Petitioner, Respondents No. 3 to 5 appropriated the same against the facilities already sanctioned to the Petitioner, which is in complete violation of the intent and purpose of the ECLGS Scheme. Pursuant to the meeting held on May 21, 2021, the Petitioner, with the intention to mitigate the stress, submitted the restructuring/revival plan to the Consortium Lenders and Respondent No. 3. However, the same was not considered or implemented by any of the lenders in accordance with the Prudential Framework.

5. It is stated that the petitioner's accounts were classified as NPA by Respondent No. 7 on December 14, 2020; by Respondent No. 6 on December 30, 2020; by Respondent No. 5 on April 1, 2022; by Respondent No. 3 on July 28, 2022; and by Respondent No. 4 on April 30, 2024. On March 30, 2022, Respondent No. 4 issued a Letter of Arrangement, under which the restructuring of the petitioner's working capital limits was allowed. On February 8, 2023, WP.No.3552/2023 titled Kotak Mahindra Bank Limited vs State Bank of India & Ors (in which the petitioner and respondents Nos. 4 to 6 have been arrayed as parties) was filed before the High Court of Karnataka by Respondent No. 7, seeking to set aside the Letter of Arrangement dated March 30, 2022, on the ground that it was issued without considering the stance/decision of Respondent No. 7. The High Court also granted an interim stay vide order dated September 20, 2023, which further derailed any restructuring endeavours. In light of the same, it is all the more necessary and pivotal that all respondents Nos. 3 to 7 be directed to jointly convene a meeting and decide on the resolution of the petitioner's debt in the light of the 2025 OTS proposal.

6. It is stated that on February 14, 2024, Respondent No. 7 issued a Show Cause Notice to the Petitioner and its directors, stating that: "your financial facilities have been unilaterally restructured without requisite approval from KMBL and without following the due process and guidelines issued by Reserve Bank of India in this aspect. Further, it was also stated that despite there being a Status-quo order by the High Court there have been blatant violations of the aforesaid orders." Thereafter, demand notices and possession notices were issued by Respondents Nos. 4 to 7. It is stated that declaring the Petitioner's asset as NPA is contrary to law. It is stated that the Petitioner, vide letter dated June 4, 2024, addressed separately to Respondents Nos. 3 to 7, highlighted the illegality in the disbursement of the GECL facility due to illegal appropriation thereof by the lenders. The Petitioner also requested the waiver of all interest charged during COVID-19 and to give the amount payable for the purpose of repayment of the outstanding amount. Respondent No. 4, vide letter dated June 15, 2024, informed the Petitioner that the GECL facility sanctioned at the time of COVID-19 had been credited to the cash credit account of the Petitioner on February 17, 2021, and the liability to that extent had come down in the said account of the Petitioner. It is stated that the action of Respondent No. 4 is in complete disregard and violation of the provisions and objective of the ECLGS.

7. It is stated that the Petitioner, vide letter dated August 5, 2024, again communicated to Respondent No. 3 its intention to resolve the debt and stated that the Petitioner would furnish a restructuring proposal that qualifies as a Resolution Plan within the meaning of the Prudential Framework. In the said letter, it is stated that a meeting of the Consortium Lenders is scheduled on August 5, 2024, at which the Petitioner will engage with the said lenders regarding the submission and consideration of a restructuring proposal. Despite all bona fide efforts by the Petitioner, Respondent No. 4 intentionally evaded replying to the Petitioner's requests. During the meeting with the Consortium Lenders held on August 5, 2024, the Consortium Lenders (who hold the majority, that is, more than 76% by value and 80% by number, as required under the Prudential Framework) decided to consider the Petitioner's resolution/restructuring plan. The action of the Consortium Lenders in not including Respondent No. 3 in the decision- making process is a sheer violation of the Prudential Framework. With the intention of keeping all the lenders at par and providing equal treatment, the Petitioner communicated the decision taken by the Consortium Lenders in the meeting on August 5, 2024, to Respondent No. 3 vide letter dated August 6, 2024. Despite being the minority lender and being aware of the decision of the Consortium Lenders (majority lender), Respondent No. 3 (through its counsel) issued a response dated August 12, 2024, rejecting the Petitioner's request regarding the consideration of the resolution plan and decided to unilaterally proceed under the SARFAESI Act. This is in violation of the Prudential Framework as well as the SARFAESI Act.

8. On August 14, 2024, petitioner issued a rejoinder to the reply dated August 12, 2024, issued by Respondent No. 3, objecting to the baseless, illegal and arbitrary reasons advanced for not considering the resolution plan. Further, Respondent No. 3 issued a letter dated August 23, 2024, stating that the decision taken by the Consortium Lenders (majority lenders) under the Prudential Framework is not binding upon them, and that Respondent No. 4, being an independent legal entity, has every right to resort to recovery measures. It is stated that the Petitioner, with the objective of resolving all its debt and catering to the interests of all lenders, while keeping Respondent No. 3 at par, submitted the debt resolution plan vide email on September 12, 2024, which provided for 100% debt repayment to all the lenders of Petitioner. It is stated that even after multiple requests and by keeping all lenders at par, Respondent No. 3, in its high- handedness, did not accord any consideration to the Debt Resolution Plan. Respondent No. 4, on behalf of the Consortium Lenders, vide letters dated September 24, 2024 (which was received by Petitioner on September 30, 2024) and October 21, 2024, conveyed the rejection of the Debt Resolution Plan and specifically directed the Petitioner to submit the resolution plan for final settlement of dues. Further, in the letter dated September 24, 2024, it was also stated that Deutsche Bank is not part of the Consortium and has to be settled separately. The timelines involved in the rejection of the Debt Resolution Plan show that the lenders have failed to apply their mind and consider the plan, and the rejection is arbitrary and unreasonable. In fact, this is further borne out by the fact that Respondent No. 4 rejected the plan immediately and sent reasons after 2 weeks vide Letter dated October 21, 2024.

9. On November 18, 2024, Petitioner sent an email to Respondent No. 3 in response to the letter dated November 11, 2024, which levelled false allegations against Petitioner. It is stated that, upon being given an opportunity to submit a one- time settlement proposal, Petitioner, vide email dated November 27, 2024, intimated Respondent No. 3 and requested that the Consortium Lenders be followed to ensure the one-time settlement proposal is constructively considered and objectively ruled on. Further, Petitioner requested that, after submission of the one-time settlement proposal, a meeting with all the lenders be convened to decide unanimously on the one-time settlement proposal. Again, an email was sent on November 27, 2024, to Respondent No. 3, requesting that the Consortium Lenders take the decision on the one-time settlement proposal together. On January 28, 2025 and February 19, 2025, petitioner addressed emails to Respondent No. 3 and the Consortium Lenders, requesting further time for submission of the one-time settlement proposal. Thus conclusion of the internal family settlement/understanding by bringing all relevant family members onto the same platform, insofar as the sale of the other property is concerned and the handling of assets/properties with interests of minors/dissenting members, is imperative to ensure the sale of the other property without any hindrance.

10. It is stated that the Petitioner also submitted the OTS Proposal dated June 14, 2025, to Respondents Nos. 3 to 7 vide its email dated June 15, 2025. Respondent No. 7 had issued a show cause notice dated September 30, 2024, asking the Petitioner why the accounts should not be declared fraudulent. The Petitioner replied to the said show cause notice on October 14, 2024, and October 19, 2024. Respondent No. 7, vide letter dated December 26, 2024, informed the Petitioner that the show cause notice dated September 30, 2024, stands withdrawn in view of the report submitted by the auditor. It is submitted that while, on the one hand, the Consortium Lenders are themselves granting the Petitioner an opportunity to submit a revised proposal (in the nature of a resolution plan), they cannot, on the contrary, proceed with recovery proceedings across judicial fora. In the event the lenders are allowed to take further actions/measures in respect of the secured assets, the same will affect the Petitioner's credibility to submit a revised resolution plan. It is stated that, despite working under the prudential norms, all the respondents have initiated several proceedings, which is contrary to the framework.

11. It is stated that, in view of coercive recovery proceedings initiated by the lenders against the children/legal heirs of Late Shree Kumar Eswar Ganjam (who was also one of the Directors of the Petitioner) at the time of devolution of guarantee obligations, and that these proceedings do not have any nexus with the business or management of the Petitioner, the children challenged the actions of the lenders before this High Court by way of filing Writ Petition No. 2212/2025. The writ petition was listed before this Court on January 30, 2025, and the Court had issued notice. It is stated that the mortgaged properties include sole dwelling residential units with minors' interests, which belong to a Hindu Undivided Family. In the event the Consortium Lenders are allowed to proceed with the sale of the other property, it would severely hamper and prejudice the interests of all the stakeholders, especially the children. It is stated that the children, being part of a Hindu Undivided Family, have an interest in the property, and their rights cannot be taken away on account of sheer non- compliance by the lenders. Hence, the petitioner has come up before this Court.

12. Learned Senior Counsel Sri. Krishnendu Datta, appearing on behalf of Sri. Manjunath C., advocate for the petitioner, submits that under Section 35A of the Banking Regulation Act, 1949, Respondent No. 1, discharging the functions of the State, is empowered to issue directions generally to banks in the public interest and in the interest of banking policy. The directions and guidelines issued by the Reserve Bank of India have statutory force and are binding, and Respondents No. 3 to 7 are required to comply with the said guidelines/circulars. He has relied on the judgment of the Apex Court in Sardar Associates vs. Punjab & Sind Bank ((2009) 8 SCC 257). It is stated that the actions initiated by Respondents No. 3 to 7 across judicial fora are in complete disregard of the guidelines issued by Respondent No. 1 and are, per se, illegal, arbitrary, and unreasonable. These actions have impinged upon, and continue to impinge upon, the fundamental rights guaranteed to the Petitioner under Articles 14, 19 and 21 of the Constitution of India. It is submitted that, on the one hand, the Consortium Lenders have granted an opportunity to the Petitioner to submit a revised proposal in the nature of a resolution plan and on the contrary, cannot proceed with recovery proceedings across judicial fora.

13. In the event the lenders are permitted to take further actions/measures in respect of the secured assets, such actions will affect the credibility of the Petitioner. Respondents No. 3 to 7 are required to collectively decide on the 2025 OTS Proposal before initiating any coercive actions against the Petitioner or pursuing the security furnished by the Petitioner to secure the debt availed from the lenders. It is submitted that the Prudential Framework requires the lenders to initiate the process of implementing a resolution plan even before a default occurs. Once the borrower is reported in default by any of the lenders, the lenders are required to undertake a prima facie review of the borrower's account within 30 (thirty) days to decide on the resolution strategy. Respondents No. 3 to 7 are also in breach of the mandatory requirement to sign the ICA within the review period. All banks were required to enter into an inter-creditor agreement pursuant to and in terms of the Prudential Framework, press release (in relation to resolution of stressed assets) by Respondent No. 2 dated July 15, 2019. Respondents No.3 to 7 have failed to comply with the Prudential Framework and instead resorted to recovery actions against the Petitioner by initiating the process of enforcement of security under the SARFAESI Act.

14. It is submitted that the actions of the lenders are in complete departure from the intent and purpose of the Prudential Framework and other applicable guidelines issued by Respondent No. 1 from time to time. All banks were required to enter into an inter-creditor agreement pursuant to and in terms of the press release (in relation to resolution of stressed assets) by Respondent No.1 dated July 15, 2019. It is stated that Respondent No. 3, despite several efforts by the petitioner to resolve the outstanding debt in a suitable manner and to bring all its lenders together for equal treatment, unilaterally initiated recovery proceedings under Section 13(4) of the SARFAESI Act, which is in complete violation of the Prudential Framework and Section 13(9) of the SARFAESI Act. It is stated that the decision taken by the Consortium Lenders, representing 75 percent by value and 60 percent by number, is binding on all the lenders, and the only option available to all lenders is to consider the 2025 OTS Proposal. The same is in accordance with the applicable guidelines issued by Respondent No. 1. However, in the truest sense, this majority threshold has not even been tested, since Respondent No. 3 was not included in the consortium-level decision-making.

15. It is submitted that while the Consortium Lenders have committed to arriving at a suitable resolution that focuses on resolving outstanding debt and ensuring the Petitioner's survival, they are simultaneously and unilaterally pursuing recovery proceedings against the Petitioner's and the guarantors' assets, which is arbitrary and unreasonable. It is submitted that despite the qualifying threshold requirement of 60 percent by number and value to initiate recovery actions under the SARFAESI Act, there was no consensus or mutual decision between the Consortium Lenders and Respondent No. 3 regarding the initiation of recovery proceedings against the Petitioner. No records have ever been produced or shared by the respondent banks showing the participation of Respondents No. 3 to 7 in the decision. It is submitted that there is a clear violation of the ECLGS scheme and non-discussion of GECL facilities. It is submitted that the respondents have failed to follow the guidelines issued by the Reserve Bank of India, Prudential Framework for Resolution of Stressed Assets (for short 'Prudential Framework'), particularly paragraph Nos. 9 and 10. In view of the same, the respondents cannot initiate any action.

16. Learned Senior counsel had relied on the judgment of the Apex Court in the case of Pro Knits Vs. The Board of Directors of Canara Bank and Others 2024 INSC 565. Paragraph Nos.13, 14 and 15 read as follows:

"13. In view of the above, it is absolutely clear that the Instructions for the Framework for Revival and Rehabilitation of Micro, Small and Medium Enterprises as notified by the Central Government vide the Notification dated 29th May, 2015 in exercise of the powers conferred under Section 9 of the MSMED Act, as revised by the RBI Notification dated 17th March, 2016, and the Master Directions i.e. the Reserve Bank of India (Lending to Micro, Small and Medium Enterprises Sector) Directions, 2016, issued by the Reserve Bank of India in exercise of the powers conferred by Section 21 and 35(A) of the Banking Regulation Act, having statutory force, are binding to all Scheduled Commercial Banks, licensed to operate in India by the Reserve Bank of India, as stated in the said Directions. It cannot be gainsaid that the Banking Regulation Act 1949 basically seeks to regulate banking business and mandates a statutory comprehensive and formal structure of banking regulation and supervision in India. Section 21 and Section 35A of the said Act empower the Reserve Bank of India to frame the policy and give directions to the banking companies in relation to the advances to be followed by the banking companies. Such directions have got to be read as supplement to the provisions of the Banking Regulation Act and accordingly are required to be construed as having statutory force and mandatory.

14. As transpiring from the said Instructions/Directions, the entire exercise as contained in the "Framework for Revival and Rehabilitation of MSMEs" is required to be carried out by the banking companies before the accounts of MSMEs turn into Non-Performing Asset. It is true that the security interest created in favour of any Bank or secured creditor may be enforced by such creditor in accordance with the provisions contained in Chapter-III of the SARFAESI Act, and that as per Section 35 of the SARFAESI Act, the provisions of the said Act have the effect, notwithstanding anything inconsistent therewith contained in any other law for the time being in force or any instrumenthaving effect by virtue of any such law. However, pertinently the whole process of enforcement of security interest as contained in Chapter III of the SARFAESI Act, could be initiated only when the borrower makes any default in repayment of secured debt or any instalment thereof, and his account in respect of such debt is classified by the secured creditor as non-performing asset, in view of Section 13(2) of the said Act.

15. What is contemplated in the "Framework for Revival and Rehabilitation of MSMEs" contained in the Instructions/ Directions stated hereinabove, is required to be followed prior to the classification of the borrower's account, (in the instant case MSMEs loan account), as Non-Performing Assets. The said Instructions contained in the Notification dated 29.05.2015 as part of measures taken for facilitating the promotion and development of MSMEs issued by the Central Government in exercise of powers conferred under Section 9 of the MSMED Act, followed by the Directions issued by the RBI in exercise of the powers conferred under Section 21 and 35A of the Banking Regulation Act, the Banking companies though may be 'secured creditors' as per the definition contained in Section 2 (zd) of the SARFAESI Act, are bound to follow the same, before classifying the loan account of MSME as NPA."

17. Relying on this, it is submitted that the guidelines issued by the Reserve Bank of India are mandatory in nature and that the respondents have failed to follow the procedure. As such, the Court is required to interfere.

18. Respondent No.1/Reserve Bank of India has filed its statement of objections. It is stated that the inter-creditor agreement (ICA) is mandatory only when lenders decide to implement a resolution plan. In all other cases, signing the ICA is not mandatory. It is submitted that the ICA shall provide that any decision agreed by lenders representing 75 per cent by value of total outstanding credit facilities (fund-based as well as non-fund-based) and 60 per cent of lenders by number shall be binding upon all the lenders. Allegations to the contrary made in the writ petition are wholly misconceived. The aforesaid directions have since been withdrawn, and their provisions have been consolidated in the recently issued Reserve Bank of India (Commercial Banks - Resolution of Stressed Assets) Directions, 2025, dated November 28, 2025. It is stated that RBI has put in place an appropriate framework and issued necessary directions/guidelines to the regulated entities on the subject matter involved in the writ petition. Banks are required to put in place Board-approved policies within the contours decided by RBI and to take commercial decisions with respect to matters concerning NPA and provision of one-time settlement. It is further submitted that there are no regulatory prescriptions prohibiting banks from engaging in recovery without exploring restructuring. Therefore, the petitioner is not entitled to any relief against the RBI, and the writ petition against the RBI is liable to be rejected in limine.

19. The representation dated April 19, 2025, states that the plan was not acceptable to the lenders. As per the Reserve Bank of India (Framework) Directions, 2019, in cases where the resolution plan is to be implemented, any decision agreed by the lenders representing 75% by value of total outstanding credit facilities (FB+NFB) and 60% of lenders by number shall be binding on all the lenders. In the instant case, the resolution plan was discussed in detail at the consortium meeting held on 20.09.2024 and was unanimously rejected. Hence, as per the RBI circular dated 07.06.2019, the company's resolution plan was not considered. It is also stated that a subsequent complaint filed by the Petitioner dated 21.07.2025 was registered in CMS as complaint number N202526023271280. As an earlier complaint (N202526023053345) from the complainant had already been dealt with on a similar matter, this complaint was closed as Non-maintainable under Clause 10(2) (b) (i) of the RB-IOS, 2021. Hence, it is stated that there has been no inaction on the part of RBI with respect to the representation dated April 19, 2025, submitted by the Petitioner. However, as the representation had alleged certain non-compliances of RBI Directions by the banks regarding misclassification of the borrower account as NPA before the due date, provisions for inter-creditor agreement, issuance of notice under SARFAESI Act, 2002, etc., the representation was reviewed from a supervisory angle, and no supervisory concerns were observed. Hence, the prayer against the RBI does not survive.

20. On 10.12.2025, this Court directed respondent No.1/RBI to file their second set of earlier objections. In those objections, they were not specific about whether all the creditors shall be part of the meeting under the Prudential Framework. As the earlier counter was not specifically answered, this Court directed respondent No.1/RBI to file an affidavit. As per the order passed by this Court, an affidavit was filed on 10.03.2026. In the affidavit, it is stated that, in order to understand the terms "all lenders", footnote 1 at page 2 of the Prudential Framework dated 7th June 2019 needs to be read:

"For the purpose of these directions, 'lenders' shall mean all entities mentioned in para 3 unless specified otherwise"

21. It is also stated that paragraph No. 9 of the said prudential framework for stressed assets would mean that once a borrower is reported to be in default by any of the lenders, all lenders shall undertake a prima facie review of the borrower's account within thirty days from such default. During this Review Period, lenders may decide on the resolution strategy, including the nature of the Resolution Plan and the approach for implementation of the RP, etc. It is further stated that in cases where RP is to be implemented, all lenders shall enter into an inter-creditor agreement (ICA) to provide ground rules for the finalisation and implementation of the RP in respect of borrowers with credit facilities from more than one lender. It is stated that, in light of the above, the Reserve Bank of India, in the instant case, respectfully submits that the framework envisages a coordinated and collective process whereby all lenders to a borrower are required to come together and undertake a review of the borrower's account within the Review Period to determine the appropriate resolution strategy. In case a Resolution Plan is to be implemented, signing of ICA is mandatory for all lenders. The ICA shall provide that any decision agreed by lenders representing 75 per cent by value of total outstanding credit facilities (fund-based as well as non- fund-based) and 60 per cent of lenders by number shall be binding upon all lenders. Additionally, the ICA may, inter alia, provide for the rights and duties of majority lenders, the duties and protection of rights of dissenting lenders, the treatment of lenders with priority in cash flows/differential security interest, etc. It is stated that, in particular, the RPs shall provide for payment not less than the liquidation value due to the dissenting lenders. Learned counsel appearing for respondent No. 1/Reserve Bank of India submits that it is mandatory that all the lenders shall come together and that this is mandatory in nature.

22. Respondent No.4/State Bank of India filed its objections, stating that the writ petition is filed by the petitioner with an ulterior motive of deceiving the public and, through clever drafting, the petitioner has tried to create an illusion of facts to bring the petition within the ambit of the writ jurisdiction of this Court, which is wrong and requires to be nipped in the bud at the hands of this Court. The petitioner has wrongly invoked the writ jurisdiction of this Court under Article 226 of the Constitution, whereas, if at all, the petitioner is aggrieved by any act of the respondent Nos.3 to 7 in holding their accounts NPA or anything wrong in issuing the demand notice, the right forum to approach is the Debts Recovery Tribunal and not this Court. It is stated that, in the entire petition, the petitioner has vehemently canvassed the contention that the respondent Nos.3 to 7 have not followed the Prudential framework guidelines and, on that score, the petitioners are seeking the indulgence of this Court in staying further proceedings of the bank in recovery proceedings. It is stated that respondent No.3 is not part of the consortium, and the petitioner has to clear the dues of respondent No.3 independently. This fact is very well within the knowledge of the petitioners. In the entire petition, the petitioner has mainly raised the issue with respondent No.3. It is stated that the petitioner recently submitted an OTS proposal for Rs. 33.50 Crores on 14.06.2025. However, compared to the outstanding balance, the proposal put forth by the petitioner was too low, and this fact was communicated to the petitioner by respondent No.4, being the lead bank, to improve the offer substantially, and the petitioner was advised accordingly vide letter dated 19.06.2025. After receipt of the said letter, the petitioner immediately hatched up the story and filed this petition.

23. It is stated that the contention of the petitioner that Respondent No. 4 has illegally slipped the petitioner's loan account into NPA is bad. It is stated that, as per the norms, the account is declared as NPA. The petitioner has raised questions regarding the Emergency Credit Line Guarantee Scheme. However, the petitioner's failure to honour the repayment of the loan cannot be attributed to the COVID- 19 pandemic, because a deep restructuring of the loan was done in March 2022, concessional interest was applied to the loan accounts, and sufficient opportunity was provided to improve the business and repay the company's loan obligations. Moreover, the Guaranteed Emergency Credit Line (GECL) of Rs.7.45 Crores was sanctioned by SBI on 28.01.2021 to mitigate financial stress. It is stated that all the banks' right to proceed against the borrower under the SARFAESI Act can be questioned only under Section 17 of the Act before the DRT, and these allegations of irregularity, if any, which this respondent strongly rebuts, cannot give any immunity to the petitioner to invoke writ jurisdiction. It is stated that the petitioner submitted the resolution plan dated 12.09.2024 to the Consortium lenders and requested the conversion of debt into sustainable debt, totalling to a tune of Rs. 30.91 Crores, which comes to 50% of the outstanding debt. In this regard, the lenders, i.e., Respondent Nos. 4 and 5 (SBI and Canara Bank), have already sacrificed huge amounts during the restructuring of the petitioner's company's credit facilities between 2022 and 2024. Respondent No. 4 has also waived interest, penal interest, and other charges, and overdue interest was converted into FITL. The respondent No. 4's right of recompense stood at Rs.6.54 Crores. Hence, at this stage, it was not feasible to consider the proposal for settlement of debt put forth by the petitioner, who was taking the lenience of the lender banks for granted. Moreover, the loan account was stamped as NPA in the books of Respondent Nos. 6 and 7 on 30.12.2020 and 14.12.2020 respectively. Hence, the plan was not accepted by the lenders.

24. It is stated that as per RBI Circular dated 07.06.2019, in cases where the Resolution plan is to be implemented, any decision agreed by lenders representing 75% by value of the total outstanding credit facilities is binding. In the guise of challenging the alleged inaction, which is not true, the petitioner seeks to create the illusion of a cause of action to invoke writ jurisdiction, but in reality, the main intention of the petitioner is to ensure that the lender banks, i.e., respondent Nos. 3 to 7, do not proceed in accordance with the SARFAESI Act. The petition filed by the petitioner is unjust and does not hold water at the test of its maintainability. It is stated that, to recover the public money, which is the paramount duty of respondent No. 4, every action of this respondent is under the purview of law. Even after receipt of all the demand notices, the petitioner has neither raised any objection against the recovery actions nor made any attempt to clear the dues.

25. The petitioner has not paid any money towards repayment of the loan since the date of NPA, which clearly shows their disinterest in clearing the dues. Now, the petitioner has filed the present writ petition on flimsy grounds, and they are doing so in a frantic effort to extricate themselves from their liability. It is stated that it has come to the bank's knowledge that during the subsistence of the mortgage, without the bank's knowledge or clearing the entire dues, the guarantor cum mortgagor, Smt. Malini Bimaji, has gifted her property to her daughter-in-law, Smt. Reshma Umesh, through a document dated 26.07.2024, registered in the SRO, Shanthinagara. It is stated that this is nothing but the mala fide tactics of the petitioner to frustrate the very process of law, and by filing the present Writ, the petitioner, instead of availing the remedy available to them, has proceeded to harass the respondent and vitiate the very framework of law.

26. Learned Senior counsel Sri. Vikram Huilgol, appearing on behalf of the learned counsel for respondent No. 4, submits that the writ petition is not maintainable. If the petitioner has any claims with regard to the proceedings initiated by the bank under the SARFAESI Act, the remedy available to the petitioner is before the Debt Recovery Tribunal under Section 17 of the SARFAESI Act, but he cannot invoke the jurisdiction of this Court under Article 226 of the Constitution of India. It is submitted that the consortium of banks led by respondent No. 4 has rejected the proposal of the respondent and Deutsche Bank, though it has not participated, that itself cannot be a ground for the Court to interfere. It is submitted that there are no grounds to interfere and the writ petition is liable to be rejected.

27. Learned Senior counsel Sri.C.K.Nandakumar, appearing on behalf of counsel for respondent No. 7, submits that in cases where RP is to be implemented, all lenders shall enter into an inter-creditor agreement (ICA) during the above- said Review Period to provide ground rules for the finalisation and implementation of the RP in respect of borrowers with credit facilities from more than one lender. Any decision agreed by lenders representing 75 per cent by value of total outstanding credit facilities (fund-based as well as non-fund- based) and 60 per cent of lenders by number shall be binding upon all the lenders. It is submitted that even if Deutsche Bank is part of the consortium and accepts the proposal, and the majority of banks do not accept it, even if there is a violation, it would not have any impact, and there is no illegality in the same. It is submitted that the petitioner only with an intention of stalling the proceedings under the SARFAESI Act, has come before this Court, and there are no grounds to interfere.

28. Respondent No.3/Deutsche Bank has not filed its objections. The other banks have adopted the arguments of the learned senior counsels appearing for respondents Nos.4 and 7.

29. Having heard the learned Senior counsel for the petitioner and the learned Senior counsel appearing for respondent Nos. 4 and 7, as well as the learned counsel appearing for respondent No. 1/Reserve Bank of India, this Court has perused the entire material on record. The bone of contention of the learned Senior counsel appearing for the petitioner is that the non-participation of Deutsche Bank in the review meeting is contrary to paragraph No. 9 of the framework. According to him, all the lenders have to participate in the review meeting and Deutsche Bank has not participated. Hence, the whole process is vitiated and contrary to the prudential framework. According to him, when the exercise under the prudential framework is pending, banks cannot take any precipitative action against the petitioner. The other contention is that the representation given to the Reserve Bank of India has not been considered, and declaring the account of the petitioner as NPA is contrary to the provisions of the Act. The property belongs to the minors, and the banks cannot initiate any action. Except for the first ground, all other grounds raised by the petitioner cannot be considered by this Court. When the bank has initiated the proceedings under the SARFAESI Act, if the petitioner is aggrieved by any of the actions, the remedy is before the DRT under Section 17 of the SARFAESI Act, and this Court is not inclined to go into any of the issues. Further, the Reserve Bank of India, in their objections, have categorically stated how they have addressed the representation of the petitioner. If any of the representations of the petitioner are not considered, a direction can be issued to the Reserve Bank of India.

30. In the light of the submissions, the issue that falls for consideration before this Court is:

"Whether the non-participation of one lender in the meetings held under the RBI Prudential Framework for resolution of stressed Assets 2019 vitiates the decision of the remaining lenders and justifies setting aside the majority decision and directing a fresh resolution process?"

31. Before going into the merits of the matter, it is appropriate to look at the "Prudential Framework for Resolution of Stressed Assets, 2019". The Prudential Framework for Resolution of Stressed Assets, 2019, by the Reserve Bank of India, has been formulated in exercise of the statutory powers conferred under the Banking Regulation Act, 1949, and the Reserve Bank of India Act, 1934. The framework is intended to secure early recognition of financial stress, timely reporting of defaults, maintenance of asset quality, adequate provisioning, and expeditious resolution of stressed exposures. The object of the framework is not merely administrative convenience, but the preservation of financial stability and regulatory discipline within the banking system.

32. The object of the framework is to ensure that the resolution of stressed assets is not stalled by individual lenders and that decisions taken by the requisite majority are given effect to in a time-bound manner. Accepting the petitioner's contention would mean that any single lender, by abstaining from participation, can frustrate the entire resolution mechanism, which would defeat the very purpose of the regulatory framework. In this case, the majority of lenders have rejected the petitioner's proposal, and if the 3rd respondent participates in the meeting and takes a contrary decision, it will not make any difference, as the majority decision will prevail. Even accepting the contentions of the learned counsel that non-participation of Deutsche Bank is bad, still it will not cause any prejudice to the petitioner. In the decision arrived at by the majority of lenders, judicial interference is not required unless there is illegality or procedural irregularity of a fundamental nature, as the decision represents the commercial wisdom of the majority of financial creditors. If a lender's conduct frustrates the framework, RBI can act through supervisory or regulatory action to ensure co- operative conduct and prevent obstruction of the collective resolution process. The Reserve Bank of India shall bestow its attention on this aspect being the regulatory authority. Non- participation by a lender in the resolution process is contrary to the spirit and object of the prudential framework. Such conduct may impede the efficiency of the resolution mechanism.

33. At this juncture, it is appropriate to look at paragraph Nos.9 and 10 of the Prudential Framework.

"9. All lenders must put in place Board-approved policies for resolution of stressed assets, including the timelines for resolution. Since default with any lender is a lagging indicator of financial stress faced by the borrower, it is expected that the lenders initiate the process of implementing a resolution plan (RP) even before a default. In any case, once a borrower is reported to be in default by any of the lenders mentioned at 3(a), 3(b) and 3(c), lenders shall undertake a prima facie review of the borrower account within thirty days from such default ("Review Period"). During this Review Period of thirty days, lenders may decide on the resolution strategy, including the nature of the RP, the approach for implementation of the RP, etc. The lenders may also choose to initiate legal proceedings for insolvency or recovery.

10. In cases where RP is to be implemented, all lenders shall enter into an inter-creditor agreement (ICA), during the above-said Review Period, to provide for ground rules for finalisation and implementation of the RP in respect of borrowers with credit facilities from more than one lender.5 The ICA shall provide that any decision agreed by lenders representing 75 per cent by value of total outstanding credit facilities (fund based as well non- fund based) and 60 per cent of lenders by number shall be binding upon all the lenders. Additionally, the ICA may, inter alia, provide for rights and duties of majority lenders, duties and protection of rights of dissenting lenders, treatment of lenders with priority in cash flows/differential security interest, etc. In particular, the RPs shall provide for payment not less than the liquidation value6 due to the dissenting lenders."

34. Paragraph No.9 of the framework envisages a structured decision-making mechanism through lender meetings under the inter-creditor arrangement, wherein decisions taken by the requisite majority of lenders in such meetings are intended to govern the resolution process. The object of the framework would be seriously undermined if individual lenders were permitted to defeat or delay a duly approved resolution plan by abstaining from meetings or pursuing parallel recovery proceedings. The petitioner's case is that the non-participation of Deutsche Bank vitiates the framework. Paragraph No.9 envisages a structural mechanism of meetings among lenders; the essence of the framework is not unanimity but majority-based decision-making under the ICA structure. The requirement of a meeting is intended to facilitate collective deliberation, but the binding nature of decisions flows from the requisite majority approval and not from universal participation or unanimity. Non-participation of a lender in such a meeting does not, by itself, invalidate the resolution process nor prevent the implementation of a duly approved resolution plan.

35. In the light of the above discussion, this Court is passing the following:

ORDER

i. This Court do not find any merit in the writ petition as far as the exercise under the Prudential Framework is concerned. Non-participation of Deutsche Bank under the Prudential Framework will not vitiate the entire process.

ii. If the petitioner is aggrieved by any of the measures taken by the Bank under the SARFAESI Act, he is at liberty to approach the Debts Recovery Tribunal.

iii. If any representations of the petitioner are pending before the respondent No.1/Reserve Bank of India, the same shall be considered in accordance with law, within a period of four weeks from the date of receipt of a copy of the order.

iv. Accordingly, the writ petition is disposed of.