Judges: THE HONOURABLE MS. JUSTICE NEENA BANSAL KRISHNA

Parties : Anju Dhawan Versus M/s. Aithent Technologies Pvt. Ltd., Through its Chief Executive Officer, New Delhi

Appearing Advocates : For the Appellant: S.C. Anand, Advocate. For the Respondent: Venancio D\'Costa, Gauri Goel, Advocates.

Date of Judgment : 16-06-2026

Head Note :-

Civil Procedure Code, 1908 - Section 96 read with Order XLI -

Comparative Citation:

2026 DHC 5120,

Judgment :-

1. The present Regular First Appeal under Section 96 read with Order XLI of the Code of Civil Procedure, 1908 (hereinafter referred to as "CPC") has been preferred by the Appellant/Plaintiff, Anju Dhawan, assailing the Judgment and Decree dated 09.04.2024, whereby the Suit for Recovery of Rs.9,09,593/- filed by the Appellant/Plaintiff has been dismissed, by the learned Additional District Judge-10, Delhi.

2. The Appellant/Plaintiff instituted the CS DJ No.13442/2016 for recovery of Rs.9,09,593/- (principal sum of Rs.3,10,500/- on account of deferred salary and compensation bonus, Rs.4,05,498/- on account of gratuity, leave encashment and other terminal dues, and interest of Rs.1,93,595/-).

3. Briefly stated, the case of the Appellant/Plaintiff was that she joined the services of the Respondent Company on 01.10.1993 and continued in employment till 22.07.2004. At the time of her resignation, she was serving as Senior Member, Consulting Staff of the Company and was drawing a gross monthly salary of Rs.83,333/-.

4. During the financial year 2002-2003, the Respondent Company faced financial difficulties on account of substantial investments in infrastructure and delayed payments from its overseas affiliated entities. Consequently, in March 2002, the Defendant Company decided to defer a portion of the salaries payable to employees drawing salaries above Rs.12,000/- per month, for the financial year 2002-2003 on a graded scale of 15%, 20%, 25% and 30% depending upon the salary range. The employees were also promised one month's salary, as bonus compensation, to offset the financial hardship occasioned by the deferment of salaries. The deferred salary was to be paid on 01.04.2003.

5. The deferment was implemented on a graded scale, and since her gross salary in March 2002 was Rs.67,500/- per month, 30% of her gross salary amounting to Rs.20,250/- per month, was deferred from April, 2002 till March, 2003. The deferred component aggregating to Rs.2,43,000/-, was agreed to be paid on 01.04.2003.

6. The Appellant/Plaintiff further asserted that, as per the policy of deferment, she was also entitled to Rs.67,500/- i.e. one month's salary, as bonus compensation. Hence, a total amount of Rs.3,10,500/- was due and payable to the Plaintiff, as on 01.04.2003.

7. Appellant/Plaintiff stated that during an Open-House Meeting held on 09.08.2002, the Management announced restoration of salaries of certain employees i.e. lowest salary group of Rs.12,000/- to Rs.20,000/- per month, with effect from 01.10.2002, and assured that the cases of other employees would also be reviewed and their deferred salaries, would be released.

8. As per the Appellant/Plaintiff, the said announcement had been made with the approval of the CEO of the Defendant Company, who had sent an e-mail dated 09.07.2002 to Mr. Raju Ahluwalia, with copies to Mr. Ajay Malik and Mr. Sunil Vadehra regarding the preponement of the decision to restore salaries to the earlier levels.

9. While the original salary of the Appellant/Plaintiff of Rs.67,500/- stood restored w.e.f. 01.04.2003, the management sought more time to pay the arrears of the deferred salary along with the compensation bonus. The Plaintiff has also relied upon a communication dated 01.04.2005, issued by the CEO of the Respondent Company assuring clearance of her dues by 31.05.2005. However, payment of the deferred salary and compensation bonus, continued to be postponed, despite repeated requests.

10. The Appellant/Plaintiff further stated that at the time of her separation, she was entitled to Car Rental of Rs.4,258/-, other reimbursements of Rs.19,476/-, Gratuity of Rs.3,05,250/- and Leave Encashment of Rs.81,694/-, while the Respondent being entitled to deduct notice period pay of Rs.5,180/-. The said terminal dues, aggregating to Rs.4,05,498/-, which became due on 23.07.2004.

11. Despite subsequent communications sent by the Plaintiff asking about her dues, including her letter dated 07.09.2005, the Respondent Company failed to release the claimed amount. The Respondent Company offered a cheque of Rs.3,96,860/- after deduction of tax of Rs.8,638/-, however, refused to disclose the details and insisted upon a receipt of full and final settlement, which was not acceptable to the Appellant/Plaintiff.

12. The Appellant thus, instituted the present Suit seeking recovery of Rs.9,09,593/- inclusive of interest (Rs.3,10,500/- towards deferred salary and compensation bonus due on 01.04.2003, Rs.4,05,498/- towards terminal dues comprising gratuity, leave encashment, car rental and other reimbursements due on 23.07.2004, and interest of Rs.1,93,595/-).

13. The Defendant/Respondent Company in its Written Statement, raised a preliminary objection regarding territorial jurisdiction, as the Appellant had been employed at the Gurgaon Office of the defendant Company.

14. On merits, it was contended that there was no deferment of salary and that the salary structure of employees had merely been restructured, in view of prevailing business circumstances.

15. The Respondent Company denied that any Agreement existed whereby the reduced portion of salary was to be repaid, at a future date. It was further asserted that the Appellant/Plaintiff herself was part of the Management team which had participated in the decision-making process relating to restructuring of salaries.

16. The Respondent Company admitted that one month's salary had been discussed as a "loyalty incentive", but asserted that the same was neither a contractual commitment nor a legally enforceable obligation, and that any such payment was contingent upon the Company achieving profitability.

17. The Respondent Company further asserted that a Letter dated 01.04.2002 had been issued to the Appellant/Plaintiff communicating the restructuring of remuneration, which letter had been signed and accepted by the Appellant/Plaintiff, without any contemporaneous protest.

18. The Respondent Company further denied that any amount remained due and payable to the Appellant/Plaintiff, at the time of cessation of her employment and prayed for dismissal of the Suit.

19. On the basis of the pleadings of the parties, the learned Trial Court framed the following Issues, on 05.10.2011:

i. "Whether this Court has no territorial jurisdiction to try and entertain the suit? Onus on parties as per their pleadings.

ii. Whether suit is not maintainable in view of preliminary objections no.2 and 3 of written statement? OPD

iii. Whether the plaintiff is entitled to amount claimed in the suit? OPP

iv. Whether the plaintiff is entitled to any interest and if so at what rate and for which period? OPP

v. Relief."

20. The Appellant/Plaintiff examined herself as PW-1 and tendered her affidavit Ex. PW-1/A. She relied upon the experience certificate dated 28.07.2004 Ex. P-1, the monthly salary certificate dated 28.07.2004 Ex. P-2, the offer letter dated 12.07.2004 from M/s Fidelity Information Systems Company India Pvt. Ltd. Ex. PW-1/1, the salary revision letter dated 30.06.2007 Ex. PW-1/2, her salary slips for the period March 2002 to May 2004 marked as Ex. P-3 to Ex. P-9 and Ex. P-11 to Ex. P-20, the Form-16 issued by the Defendant for the Assessment Years 2002-03 to 2005-06 marked as Ex. PW-1/3 to Ex. PW-1/6, the letter dated 01.04.2005 issued by the CEO of the Respondent Company Ex. P-10, her own letter dated 07.09.2005 Ex. PW-1/7, and the postal receipts Mark PW-1/A.

21. PW-2, Shri Sunil Vadehra, former Director and Head of India Operations of the Respondent Company, who deposed about the e-mail dated 09.07.2002 and connected correspondence Ex. PW-2/1 (coll).

22. DW-1, Shri Banty Bisht, Manager (HR) of the Defendant Company, who proved the copy of the Minute Book Ex. DW-1/A. The deposed about the defence as stated in the Written Statement.

23. The learned ADJ, upon appreciation of the evidence led by the parties, concluded that the Appellant/Plaintiff had failed to establish any contractual arrangement, whereby the reduced component of salary was to be repaid at a later date or that one month's salary was contractually payable as bonus. Consequently, the Suit was dismissed vide Judgment and Decree dated 09.04.2024.

24. Aggrieved by the said Judgment and Decree dated 09.04.2024, the present Appeal has been preferred by the Appellant/Plaintiff.

25. The grounds of challenge primarily are that the learned ADJ erred in dismissing the Suit despite the documentary record, particularly the e-mail dated 09.07.2002 Ex. PW-2/1, consistently employing the terminology "deferred salary", establishing that the salary reduction during the financial year 2002-2003 was a deferment and not restructuring.

26. It is further submitted that the impugned Judgment is self- contradictory inasmuch as the learned ADJ has placed reliance upon the decisions in Dale & Carrington Invt. (P) Ltd. v. P.K. Prathapan, (2005) 1 SCC 212 : 2004 SCC OnLine SC 1067, and Mukesh Hans v. Uma Bhasin, 2010 SCC OnLine Del 2776, to underscore the importance of a Board Resolution, while overlooking that admittedly no Board Resolution exists authorising the salary reduction either as a deferment or as a restructuring; that the said decisions pertain to internal disputes amongst shareholders and personal liability of Directors and were inapplicable to the facts in hand. In the present case, the communication dated 01.04.2005 Ex. P-10 issued by the CEO of the Respondent Company, established the case of the Appellant/Plaintiff.

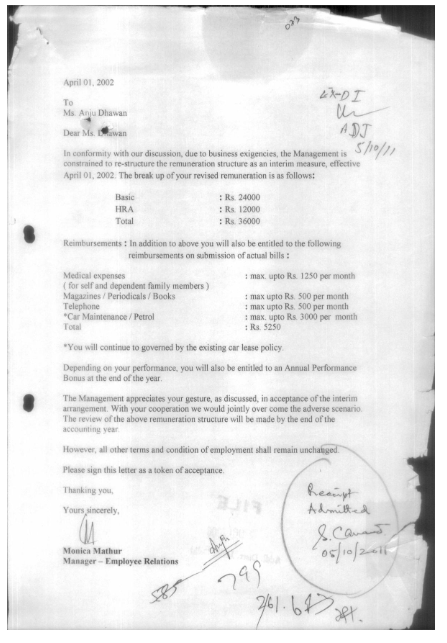

27. It is also stated that the learned ADJ failed to address the issue of interest on the terminal dues of Rs.3,96,860/-, which had accrued on 23.07.2004 which were paid only during the pendency of the Suit, in three instalments, the last being paid on 05.10.2011, accepted without prejudice; and that a balance sum of Rs.9,838/- remained unpaid.

28. The Appellant has accordingly, prayed that the impugned Judgment and Decree dated 09.04.2024 be set aside and the Suit be decreed.

29. The Respondent, in its Short Note of Submissions, has contended that the salary reduction during the Financial Year 2002-2003 was a restructuring of remuneration, necessitated by the financial constraints faced by the Company in the aftermath of the events of 11.09.2001, and was not a deferment of salary. This is evident from the communication dated 01.04.2002 Ex. D-1 itself, which referred to restructuring as an "interim measure", it did not contain any promise for repayment on a future date.

30. It is further submitted that the Appellant, who continued in service even after restoration of salary w.e.f. 01.04.2003, did not raise any contemporaneous claim for the alleged arrears. The reliance has been placed upon the Judgment dated 06.08.2018 passed by Co-ordinate Bench of this Court in M/s Aithent Technologies Pvt. Ltd. v. Archana Verma (RFA 608/2014), wherein claims arising out of the salary restructuring exercise were dismissed, which Judgment has attained finality. Submissions heard and Record perused.

31. It is the case of the Plaintiff/Appellant, Ms. Anju Dhawan, that she joined the Defendant Company, as Senior Member, Consulting Staff on 01.10.1993 and continued in service until 22.07.2004, when she tendered her resignation, which was duly accepted by the Defendant Company.

32. She further deposed that at the time of her separation, she was drawing a gross monthly salary of Rs.83,333/-, as recorded in the Salary Certificate dated 28.07.2004 Ex. P-2, issued by the Defendant. The factum of her employment for the period 01.10.1993 to 22.07.2004 is further confirmed by the Experience Certificate dated 28.07.2004 Ex. P-1, which records that the Appellant "has left the services of our organisation on her own accord." The Plaintiff further deposed that prior to the events giving rise to the present dispute, she was drawing a gross monthly salary of Rs.67,500/-, comprising Basic of Rs.37,500/-, House Rent Allowance of Rs.18,750/- and reimbursements aggregating to Rs.11,250/-, as is borne out by the Salary Slip for March 2002 Ex. P-3. These facts are admitted by the Defendant Company.

33. The entire controversy in the present case, centres around the reduction of the Plaintiff's salary during Financial Year 01.04.2002 till 31.03.2003. It is an admitted position that with effect from 01.04.2002, the Plaintiff's Basic and House Rent Allowance components were reduced from Rs.56,250/- per month to Rs.36,000/- per month, and continued until 31.03.2003. It is further undisputed that with effect from 01.04.2003, her Basic and House Rent Allowance components, were restored. Thus, there was an admitted reduction of Rs.20,250/- per month in the Plaintiff's salary for one year i.e. the period from 01.04.2002 to 31.03.2003, aggregating to Rs.2,43,000/-.

34. The circumstances leading to reduction in salary for Financial Year 2002-03, were explained by the Plaintiff in her testimony and corroborated by PW-2 Sh. Sunil Vadehra, then Director and Head of India Operations of the Defendant Company. It was stated that the Defendant Company faced a severe liquidity crunch on account of substantial investment in infrastructure during the year 2001, accentuated by delay in receipt of payments from its affiliated entities namely Velos, Canyon Blue and Zero to N.

35. Towards the end of March, 2002, discussions were held within the senior management of the Defendant Company, comprising Mr. N. Venu Gopal (CEO), Mr. H.R. Ahluwalia (Vice President - HR), Mr. Sunil Vadehra (Director and Head of India Operations), Mr. Sanjay Verma (Vice President - Technology) and Mr. Rajeeva Gupta (Associate Vice President - Technology). It was thereafter, decided that an Open House Meeting of all employees be convened to share the prevailing situation and seek their cooperation.

36. The proposed measure involved deferment of a portion of the employees' salaries on a graded scale for a period of up to twelve months. It was represented that upon expiry of the said period, the salaries would be restored to their original levels. The management also promised a special bonus equivalent to one month's salary to each employee.

37. As per the Plaintiff, under the aforesaid arrangement, the Defendant Company agreed with employees drawing a gross salary above Rs.12,000/- per month to defer a portion of their salary for Financial Year 2002-2003, till April 2003. The deferred portion of the salary was determined on a graded scale, namely 15%, 20%, 25% and 30% for employees drawing gross monthly salaries in the ranges of Rs.12,000/- to Rs.20,000/-, Rs.20,000/- to Rs.30,000/-, Rs.30,000/- to Rs.60,000/- and above Rs.60,000/- respectively.

38. Consequently, the amount of deferred salary attributable to the Plaintiff for Financial Year 2002-2003, on the 30% slab, was Rs.2,43,000/-. Upon adding the promised bonus equivalent to one month's salary of Rs.67,500/-, the Plaintiff claimed that a total sum of Rs.3,10,500/- became due and payable to her, which was not paid by the Defendant Company.

39. The Defendant Company, on the other hand, contended that the arrangement was not one of deferment of salary and that no promise had been made to pay the reduced salary amount with effect from 01.04.2003 to the employees. In fact, owing to the financial difficulties being faced by the Company, the salaries of employees were restructured for a period of one year. It was, therefore, asserted that there was no question of any deferred salary becoming payable to the Plaintiff or any other employee.

40. The first significant document is Letter dated 01.04.2002 Ex. D-1, issued by the Defendant Company to the Appellant/Plaintiff at the very inception of the disputed arrangement. The said document is the only contemporaneous communication addressed individually to the Appellant by the Defendant Company, about the salary reduction, and is admittedly signed by the Appellant in acknowledgement of acceptance. The same is reproduced as under:

41. Significantly, the said document characterises the modification of remuneration as a "re-structure" and as an "interim measure", and is completely silent on any deferment of salary or on any obligation undertaken by the Defendant Company to repay the reduced component of salary at a future date. The Plaintiff has admittedly signed the said document and has admitted her signatures on the Letter, in her cross-examination, conceding that she did not give any objections regarding Ex. D-1 to the Defendant Company in writing. There is no recital of conditional acceptance on the face of the document.

42. The admissions made by the Plaintiff further reveal that there was no formal written Agreement, Board Resolution or other contemporaneous document, recording any obligation on the part of the Defendant Company to repay the reduced salary at a future date. The Plaintiff specifically conceded in her cross-examination that at the time of restructuring, no objection in writing was given by her to the Company; that during her entire period of service she never gave any Letter regarding restructuring of her salary; that there was no written letter given by the Defendant Company regarding payment of the restructured/deferred salary; and that she could not produce any document regarding the deferred salary having been paid to any other employee.

43. The Plaintiff has placed reliance upon the e-mail dated 09.07.2002 Ex. PW-2/1, addressed by the CEO of the Defendant Company to the Vice President HR, which uses the terminology "deferred salary". However, the said e-mail is an internal management communication, not addressed to or signed by the Appellant. The only document communicated to and signed by the Appellant on the subject of the salary reduction is Ex. D-1, which characterises the arrangement as a "re-structure". Internal management correspondence, cannot displace the express terms of the written contract between the parties.

44. The e-mail dated 09.07.2002 contemplated partial reversal of the deferment decision, only for the lowest salary slab. For the higher slabs to which the Appellant belonged, it stated that the cases "would be reviewed at the end of the next quarter and implemented gradually" language of future contemplation rather than of present commitment. No subsequent communication crystallised the said contemplation, into a binding obligation.

45. Another aspect which is of immense importance, is that the Plaintiff continued in service of the Defendant Company for over fifteen months, after the alleged date of accrual of the deferred salary on 01.04.2003, and ultimately resigned on 22.07.2004. The Experience Certificate Ex. P-1 records that she left the services "on her own accord." If it was indeed a case of deferment, there is no reason why she would not have protested, insisted or claimed her outstanding dues at the time of her resignation, particularly since the alleged due date of 01.04.2003 had passed well over a year earlier.

46. The conduct of the Plaintiff, in not claiming any outstanding dues at the time of her resignation, and her filing of the Suit only on 01.04.2006, also lends support to the conclusion that it was not a formally agreed policy of the Defendant Company, to pay the deferred salary.

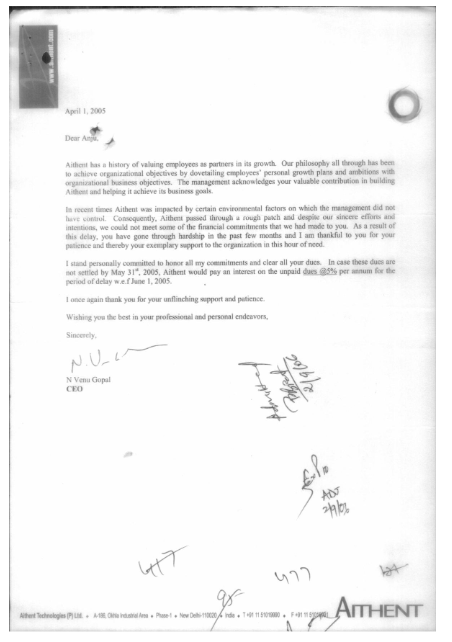

47. The Appellant/Plaintiff has also placed reliance upon the letter dated 01.04.2005 Ex. P-10, wherein the CEO of the Respondent Company stated that he remained committed to clear the dues of the Appellant/Plaintiff. The same is reproduced as under:

48. However, the said communication neither quantifies the alleged dues nor identifies their nature. There is no reference to the reduced salary for Financial Year 2002-2003, no mention of any compensation bonus and no recital that the salary reduction was merely a deferment to be repaid at a future date.

49. It is not disputed that there were discussions regarding payment of a one month's salary bonus to employees. However, the Appellant/Plaintiff has failed to place on record any material to establish that the said bonus crystallised into a binding contractual obligation. The consistent stand of the Respondent has been that the same was contemplated only as an incentive and not as a legal commitment. In the absence of any document or other cogent evidence demonstrating that the bonus became payable as a matter of right, the claim towards compensation bonus cannot be sustained.

50. The Plaintiff has relied upon the aforesaid two communications, but from these, there is no admission of there being any deferment of salary or the entitlement of the Plaintiff for the same.

51. The learned Trial Court has carefully appreciated the evidence brought on record and has rightly concluded that while reduction of salary during the relevant period stands admitted, the Appellant/Plaintiff failed to establish that such reduction merely constituted a deferment creating a legally enforceable obligation to repay the amount at a later date.

52. Significantly, during the pendency of the Suit, the Respondent admitted its liability towards the terminal dues of the Appellant/Plaintiff on account of gratuity, leave encashment and connected dues, and vide Order dated 12.01.2011 was directed to pay a sum of Rs.3,96,860/- (being Rs.4,05,498/- less statutory tax deduction of Rs.8,638/-). The said amount was paid in three instalments, namely, Rs.1,50,000/- on 29.03.2011, Rs.1,50,000/- on 06.07.2011 and Rs.96,860/- on 05.10.2011, and was accepted by the Appellant/Plaintiff. The said terminal dues, accordingly, no longer survive as a live dispute in the present Appeal, and the claim now pressed in the Appeal, is confined to interest on the said paid amount

53. The Appellant has, in the present Appeal, pressed a claim for interest at 12% per annum on the said sum of Rs.3,96,860/- from the date of accrual on 23.07.2004 till the respective dates of payment, on the strength of the assurance contained in the letter dated 01.04.2005 Ex. P-10.

54. The said claim cannot be sustained for the simple reason that the Appellant had been offered this amount, and the Respondent Company had offered a cheque of Rs.3,96,860/- after deduction of tax of Rs.8,638/-, in September, 2005. However, the appellant herself had declined to accept it.

55. The Plaintiff's claim of a balance unpaid sum of Rs.9,838/- on account of Provident Fund, Leave Encashment and connected dues is equally untenable. The Appellant has not placed on record any computation establishing the said balance. The Respondent has paid Rs.3,96,860/- in satisfaction of admitted terminal dues of Rs.4,05,498/-, the differential of Rs.8,638/- representing the statutory tax deduction at source. No further amount stands established on the record.

56. The terminal dues of Rs.4,05,498/- having stood satisfied by payment of Rs.3,96,860/- to the Appellant, during the pendency of the Suit (after statutory deduction of tax of Rs.8,638/-), and the claims on account of interest on the said paid amount, and the alleged balance sum of Rs.9,838/-, having been found to be unsustainable for the reasons recorded hereinabove, no further direction is called for on this account.

57. There is no merit in the present Appeal, which is hereby, dismissed along with pending Applications.